Jun 28, 2026

Harvey Was Founded Knowing the Models Would Become Its Competitor

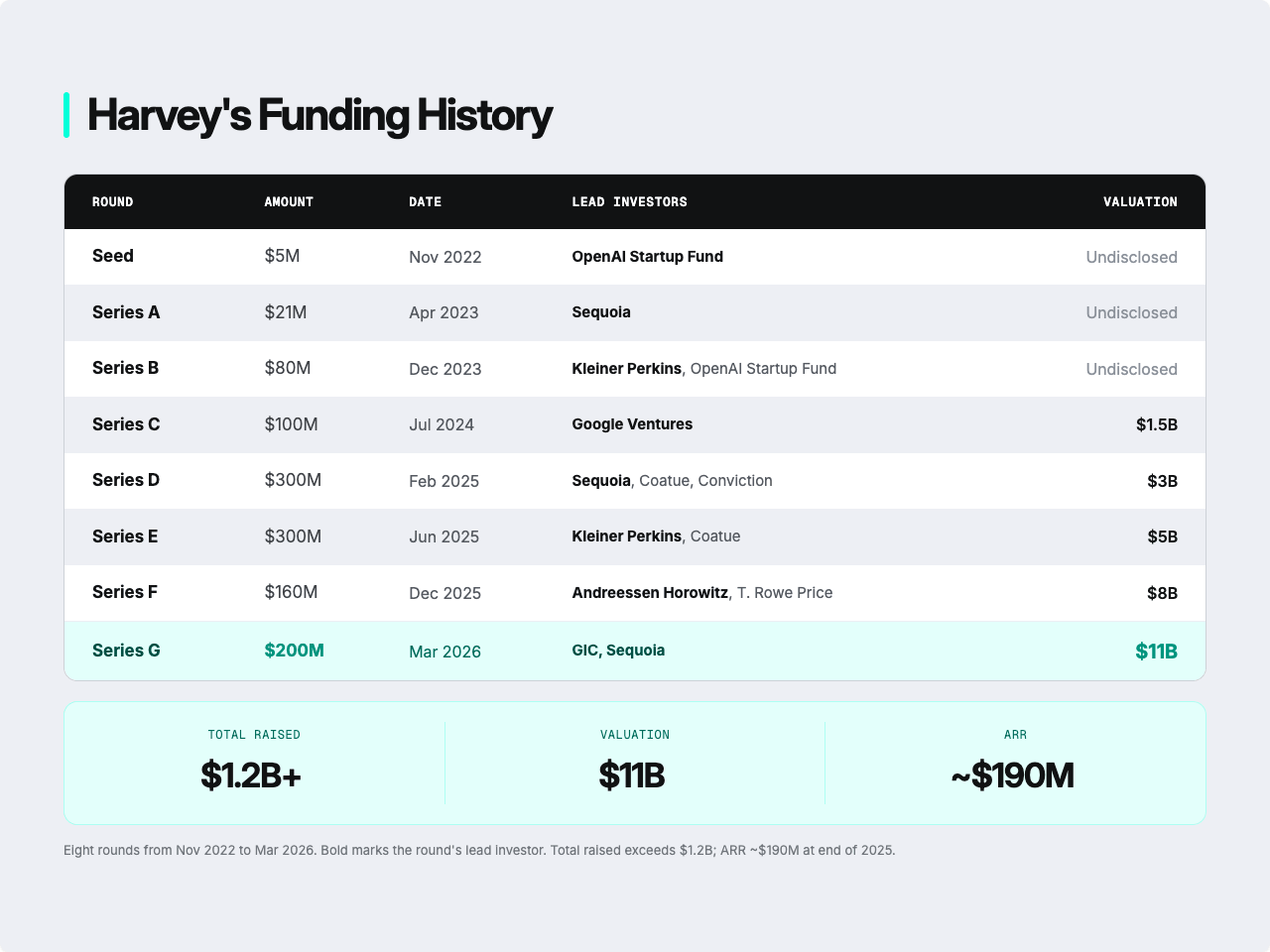

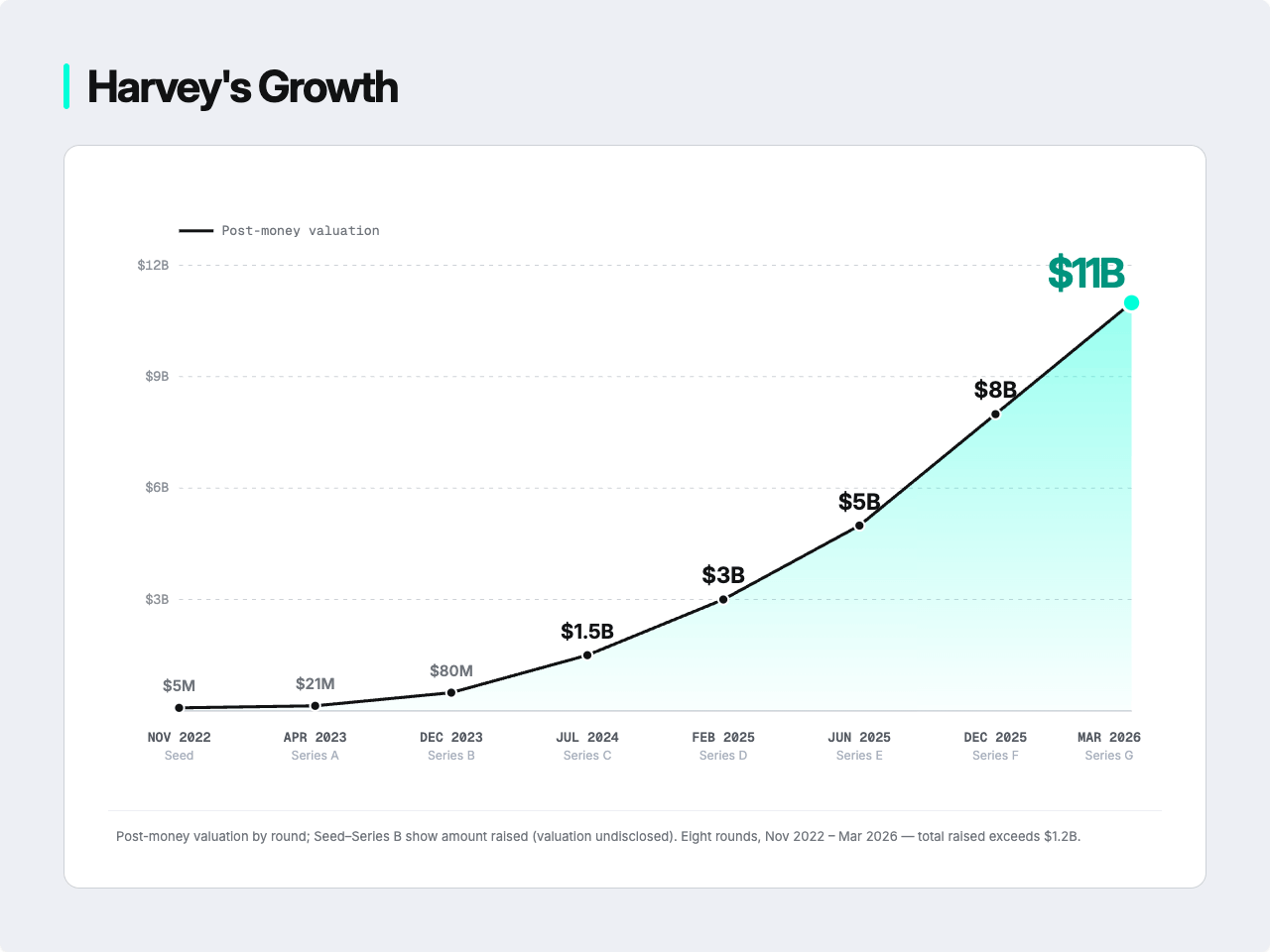

Breaking Down Harvey's Series G

Raise Report

0:00 / 0:00

💡

At a Glance

- Company: Harvey, a legal AI platform for law firms and in-house teams

- Co-founders: Winston Weinberg (CEO) and Gabe Pereyra (President)

- Funding: ~$200M at a ~$11B valuation (March 2026), led by Sequoia with GIC; the OpenAI Startup Fund anchored the 2022 seed

- Investors: OpenAI Startup Fund, Sequoia, Andreessen Horowitz, GIC, Kleiner Perkins, Conviction, Elad Gil, and others

- Growth: ~$190M ARR (end of 2025); 1,000+ customers; more than half of the Am Law 100

- Key product: Multi-model legal platform, with Vault, Shared Spaces, and an open legal benchmark

What Everyone Realized in 2026, Harvey Knew in 2022

In February 2026, Anthropic shipped a legal plugin for Claude, and legal tech stocks fell hard. The fear behind the sell-off is easy to state. If the model keeps getting better at everything, then every company built on top of one is a thin wrapper waiting to be absorbed, and the only value left standing is the compute and the frontier weights. Sarah Guo of Conviction called it the mid-2026 version of investor despair in her essay, 'The Untrainable.'

None of it was news to Harvey. It had been the company's premise for four years. Winston has said they built the company from the start on the belief that the model labs, not rival legal startups, were the competitor that mattered, something Gabe Pereyra had carried over from his years as an AI researcher.

"Our largest competitor is by far, indirectly, OpenAI."Winston WeinbergCo-founder & CEO of Harvey

So the sell-off that shook the rest of the category landed on Harvey, the one company that had been standing in its path the whole time.

A month later, Harvey raised $200 million at an $11 billion valuation, in a round led by Sequoia with GIC.

That is the whole puzzle. Harvey saw the threat first, built around it longest, and got paid the most for it. Which is exactly what makes the obvious question hard to answer. Did those four years of treating the model as the enemy build something that can actually be defended? Or did Harvey just panic earlier than everyone else?

A Hot Category, and the Target Painted on First Place

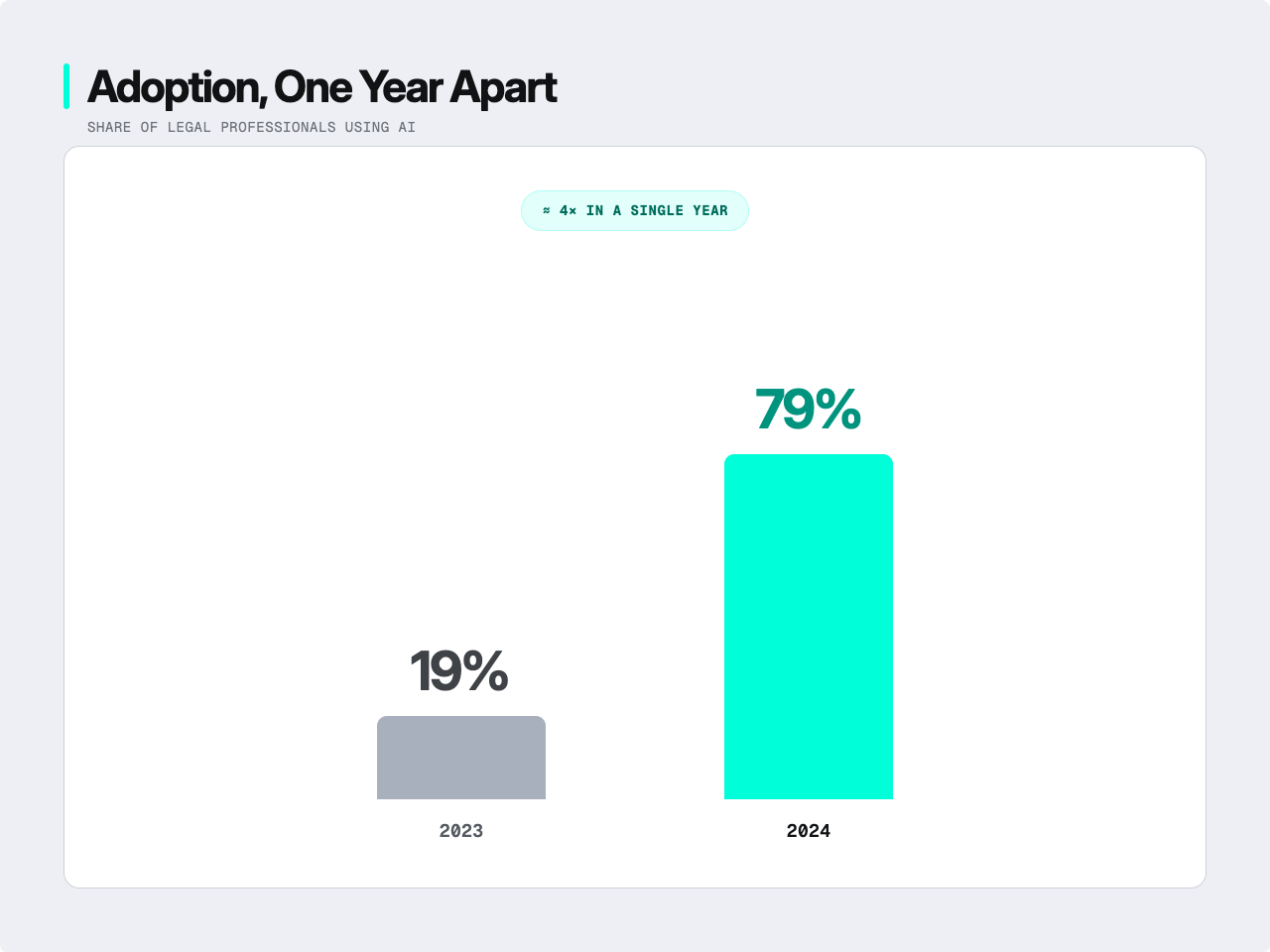

Everyone is aiming at the "legal AI" category for a simple reason. It is huge and almost untouched. The legal market is worth roughly a trillion dollars, and only about thirty billion of that goes to technology. There are around ten million legal professionals in the world. Adoption is moving fast: the share of them using AI jumped from 19 percent in 2023 to 79 percent in 2024, and legal tech funding hit 3.2 billion dollars in 2025.

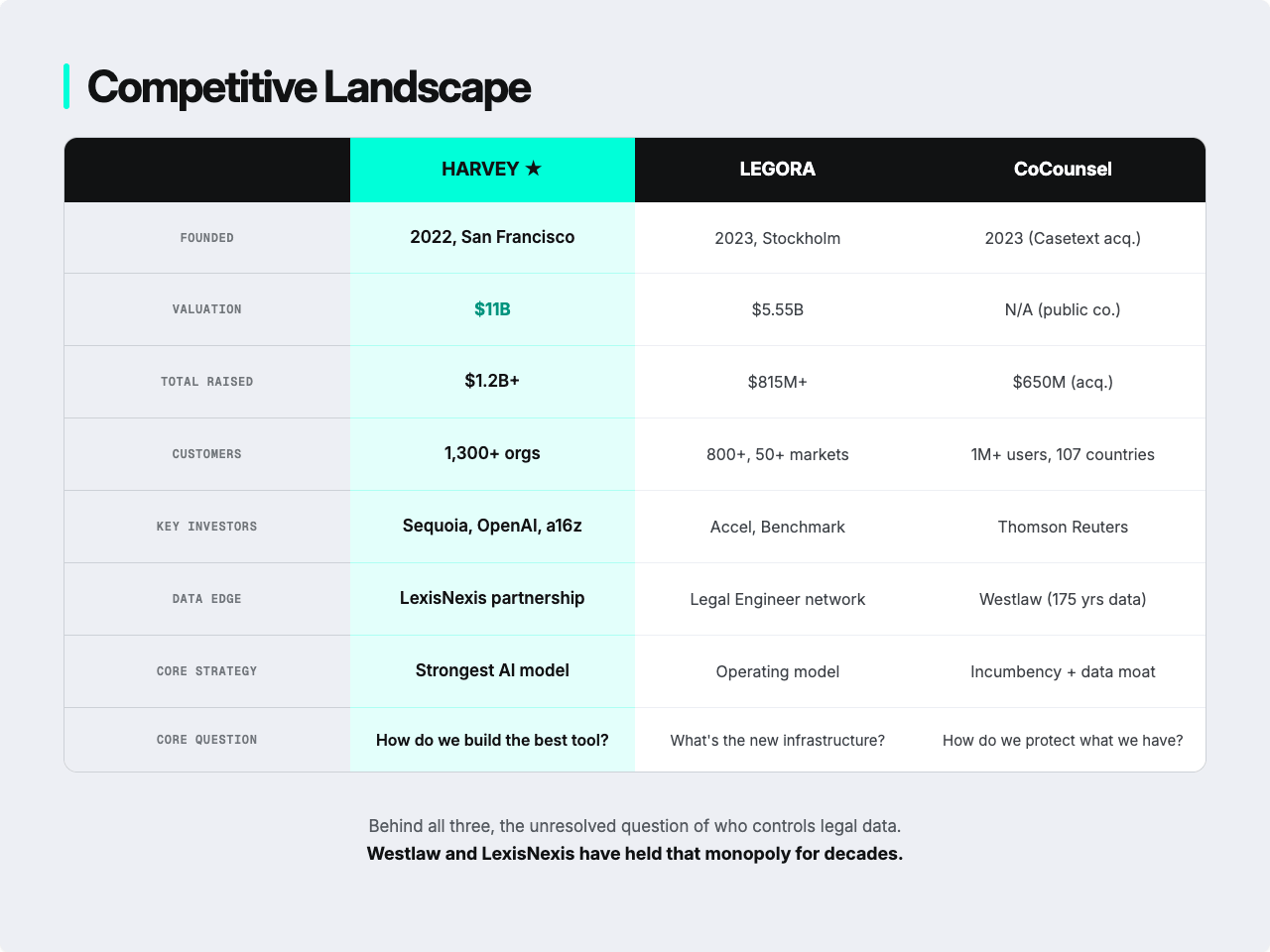

Inside that category, Harvey leads by almost every conventional measure. Annual recurring revenue is around 190 million dollars. It has more than a thousand customers, more than half of the Am Law 100 among them. It placed first overall in VLAIR, the most cited independent benchmark for legal AI. Its sales team is built from former lawyers at White & Case, Latham, Skadden, and Paul Weiss, a two-year head start in relationships that rivals are still trying to close.

Elad Gil, who is on the cap table of nearly every notable AI company of the past decade, has a warning about numbers like these. In AI, fast revenue can be a mirage, because enterprises run trials they may never commit to.

"There's false signal, and then there's stuff that is just working."Elad GilSolo Investor

He puts Harvey in the second column.

But first place is also the biggest target, and to understand why, look at how the ground just shifted. In the old version of this market, the moat was data. Thomson Reuters had it, building CoCounsel on Westlaw's 175 years of legal records and reaching a million professionals by early 2026. LexisNexis had it too, and Clio paid a billion dollars to buy vLex outright. The conventional read was that whoever controlled the data controlled the category.

Harvey took that axis off the table, not by out-collecting the incumbents but by buying its way in. Its 2025 partnership with LexisNexis put authoritative primary law straight into the product, and the data giant became a supplier instead of a rival. Legora, Harvey's biggest rival, went the other way and stayed out of the data race entirely, betting the value was never there to begin with. Neither company treats data as the main battleground anymore.

The model is. And that is exactly the front Harvey said it would fight on four years ago, which sharpens the question instead of settling it. Being the largest application-layer company in legal AI also means being the most exposed when the labs reach down into the layer above them. First place here is not proof of safety. It is proof of exposure.

So before deciding whether the lead will hold, look at what Harvey actually built while betting the models would come for it.

What Four Years of Betting on the Models Built

Before judging whether Harvey built a moat or just flinched early, it is worth laying out what those four years actually produced.

Harvey was multi-model from the start, and by design. The reasons were structural, not only about performance. A firm representing OpenAI cannot send that client's data to Anthropic. Meta wants its outside counsel on Llama. Different models turn out to be better at different legal tasks. And there is the plain risk of depending on any one lab. As Pereyra put it in an interview with EO:

"I don't think you can bet on a single model provider because they could run out of compute, they could fall behind in the model race."Gabe PereyraCo-founder & President of Harvey

On top of that, it routes to cheaper models once accuracy is high enough, and post-trains open-source models on its own eval sets.

It was built for the institution rather than the individual. The aim is organizational productivity, the layer that the founders argue the model providers will not bother to build while they perfect single-user tools.

It tied accuracy to partner approval. The working test is whether a partner would sign off on the work product before sending it to a client, with firm-specific and practice-specific eval frameworks layered on top. It publishes its own legal benchmark.

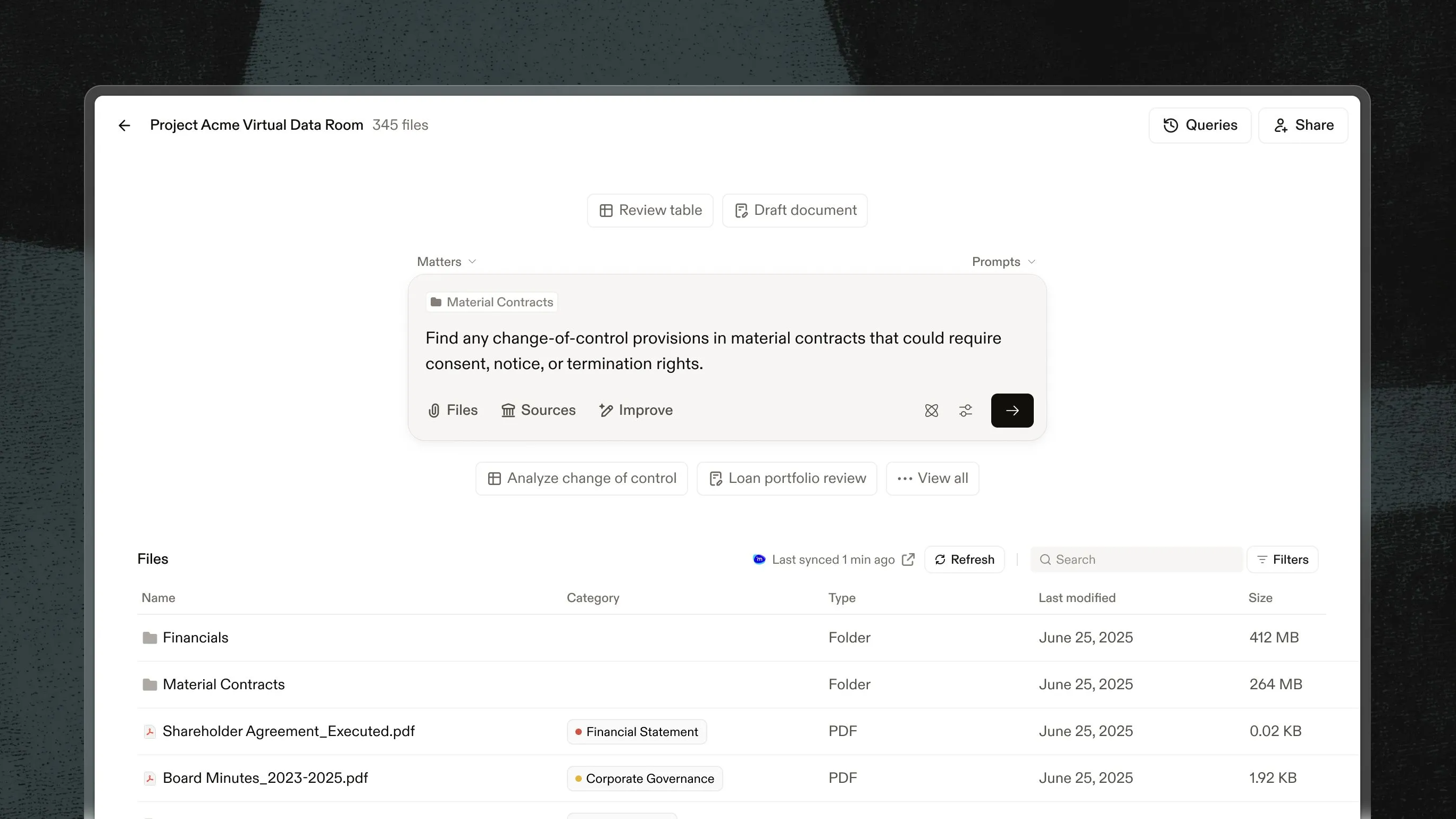

It pushed deep into the firm. The encrypted Vault uses retrieval-augmented generation to cite a firm's own documents. The Lighthouse program co-developed the platform inside firms like Allen & Overy and PwC. Shared Spaces puts a firm and its client in a single workspace. A Memory feature is being built together with the industry.

It sold from the top down. Against the standard advice, Harvey went after the largest firms first. Four people took shifts to onboard Allen & Overy Sherman's four thousand lawyers. Demos were personalized to the point of attacking a lawyer's own recently filed brief, live, in the room.

And the numbers followed. Daily return usage is up 81 percent since 2023. A fifth of users are partners, even though only 18 percent of Harvey's own staff are lawyers. PwC partners reportedly said their junior lawyers would riot if the tool were taken away.

One reading calls this list a moat. The other calls it a set of features anyone can copy. Here is the strongest version of each.

The Case That Harvey Built Something Real

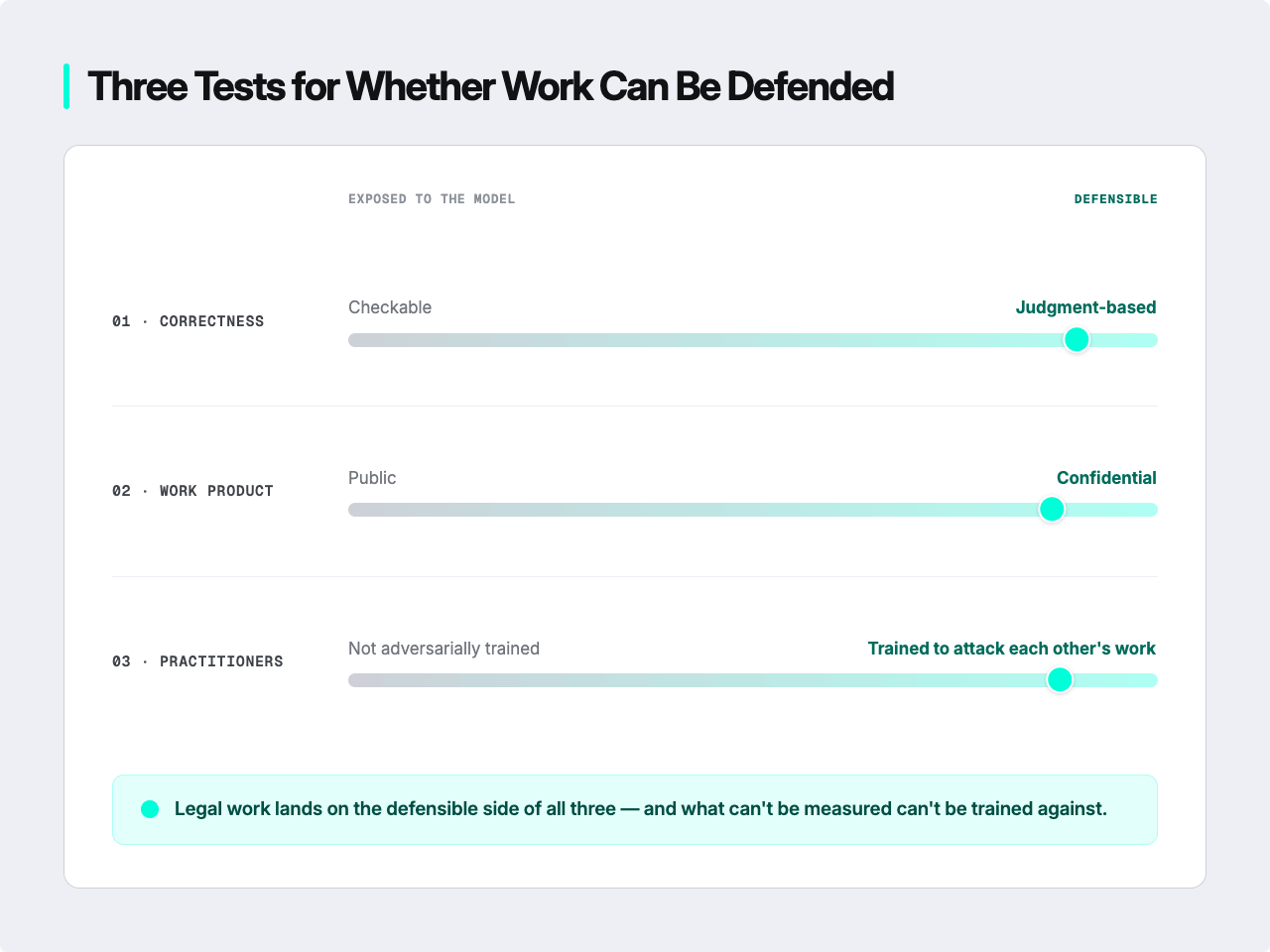

The strongest version of the bull case has nothing to do with Harvey's brand or its revenue. It rests on a claim about legal work itself, and you can test that claim with three questions. Is the work's correctness checkable, or is it a matter of judgment? Is the work product out in the open, or locked inside someone's confidential files? And are the people who do it trained to tear each other's work apart? On all three, law leans toward defense.

Take judgment first. You can read a contract and confirm every clause is written correctly, Pereyra notes, but the real test is whether the merger it enabled is still standing ten years later. Judging a top partner is like judging a venture capitalist. He explained it this way to EO:

"There is no multiple choice test... you look at their track record for 20 years."Gabe PereyraCo-founder & President, Harvey

You look at the deals that closed and the cases that were won, over twenty years. Work like that cannot be read off a leaderboard. And anything that cannot be measured cannot be trained against, which is exactly why the most valuable legal judgment sits beyond the reach of the models.

Confidentiality is the second test. A smarter model still cannot do fund formation, Weinberg points out, because that data does not exist on the internet. It lives inside specific client relationships and private datasets. At a white-shoe firm the M&A practice alone can run close to a thousand deals a year, and the signal that matters sits at the level of the deal, not the single document. You cannot hand that to a general-purpose agent, for confidentiality reasons and a dozen more.

The third is the authority to evaluate. When work cannot be scored from outside, someone on the inside has to decide what a good answer even looks like, and enough of those decisions, written down, become a benchmark. That authority tends to stay where it already lives. Harvey publishes a legal benchmark. The labs' own benchmarks, meanwhile, are becoming useless for a vertical. What a firm needs is an eval for this kind of fund, with this many LPs, across seventy jurisdictions, and no lab can write that, however smart its model gets.

Put the three together, and the threat looks different. A better model does not hold the license, sign the liability, own the firm's files, or stand in court when the answer is wrong. The bottleneck was never intelligence. It is permission, and it is accountability. There is a lock on the door, the environment you only get into after the security review and the contract, and there is a deadbolt behind it, the user's daily habit that no amount of computing can buy.

This is why getting embedded matters so much. Move into these systems fast enough, Winston argues, and partners will not want to rip them out. And because Harvey serves both sides of the market, the firm and its client are pulled into the same workspace through Shared Spaces, making it harder for both to leave.

Read this way, Gabe's line about worrying too much about the moat being one of their biggest mistakes is not an admission that there is no moat. It is a claim about order. Nobody predicted network effects when the Internet showed up, either. You do not design the moat up front. It forms while you solve customers' problems at scale.

The Case That They Just Panicked Earlier

The best witness against Harvey is not a competitor. It is Harvey's own founders.

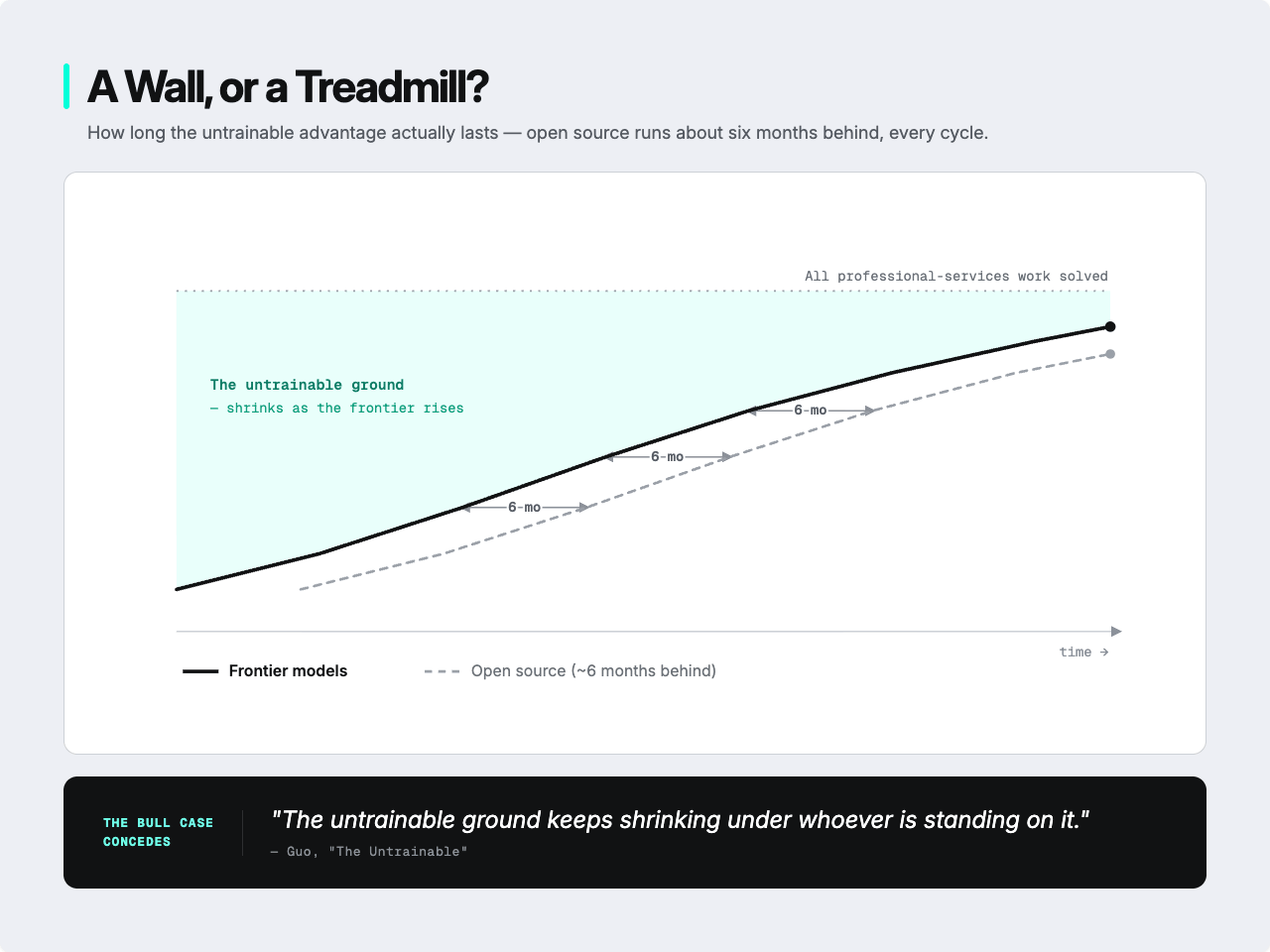

Consider how long the advantage actually lasts. Open source runs about six months behind, Pereyra says, and he is blunt about it. If the models ever solve all of professional services work, open source does the same thing half a year later. Hold that against the bull case, and the untrainable corner stops looking like permanent ground. It looks like a six-month lead you have to win every cycle again, less a wall than a treadmill. Guo's 'The Untrainable,' the clearest statement of the bull case, concedes this when it says the untrainable ground keeps shrinking under whoever is standing on it.

Then there is everything Harvey built, the list, the bull case called a moat. Every item on it is being copied right now. Multi-model routing is table stakes. The move from single-user to institutional, what the founders call "organizational productivity," is the stated goal of every serious player in the category, Harvey included.

The shared firm-and-client workspace Harvey shipped as Shared Spaces, Legora shipped the same month as Portal, on the opposite assumption: Harvey treats it as co-creation, Legora as productization, with the firm packaging its own expertise and selling it under its own brand. Two companies shipping competing takes on the same thing within weeks of each other looks less like a defensible advantage than like a feature race.

The moat-as-order argument is the weak link, and it is weak for a specific reason. Nothing could ever prove it wrong. The claim is that you should not design a moat up front because one forms while you solve problems at scale. But a moat that forms and a moat that never forms are described by the very same sentence. A claim that survives every possible outcome is not evidence of anything. It is faith stated after the fact, and faith does not defend a business.

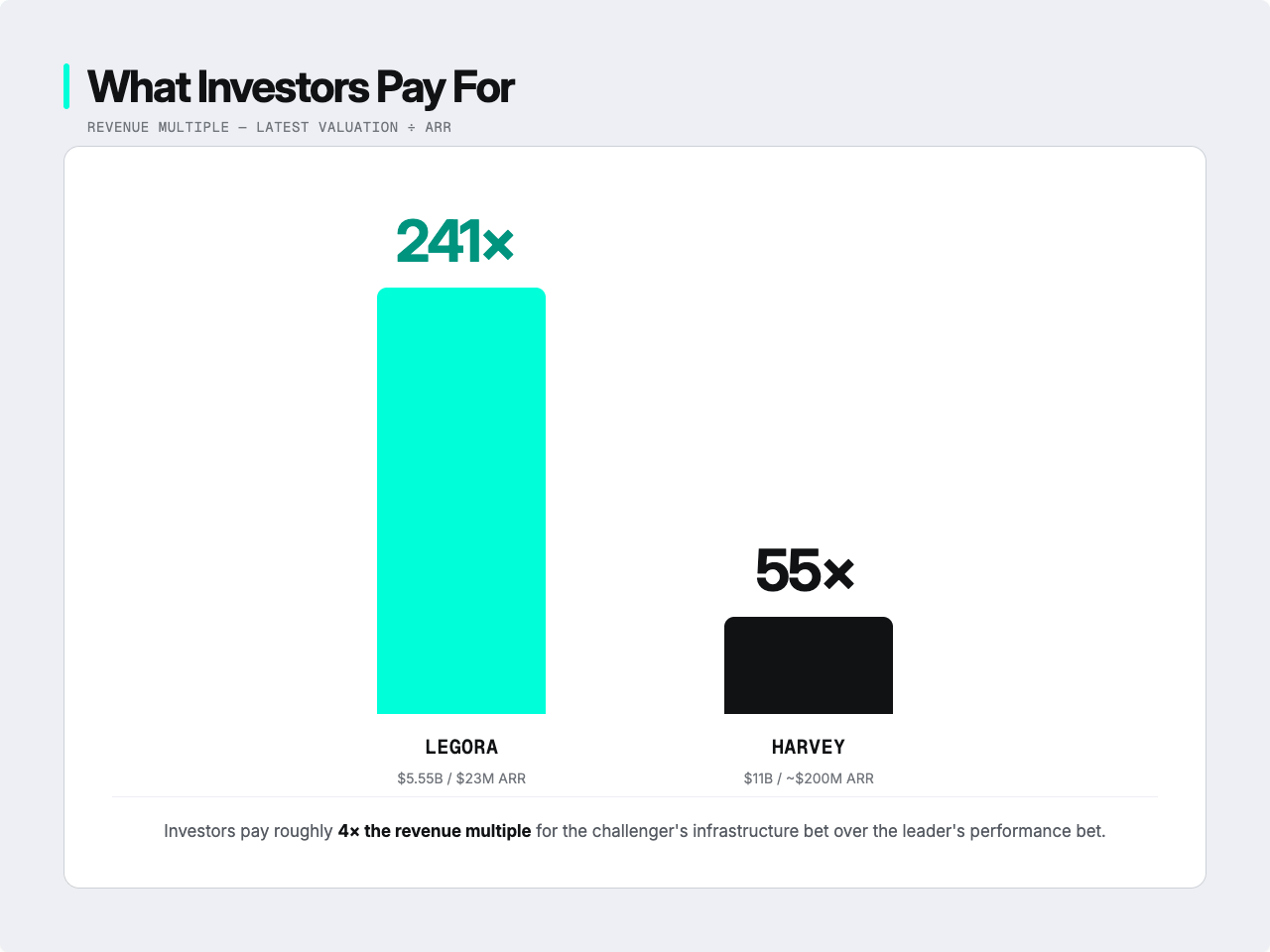

Look at the market, too. Legora trades at roughly 241 times revenue, based on its $ 5.55 billion valuation. Measured the same way, against an $11 billion valuation and revenue of around 200 million, Harvey trades at about 55. Investors are paying a steep premium for the challenger's infrastructure bet over the leader's performance bet, which is another way of saying they do not treat first place and a durable position as the same thing. Legora is closing the gap faster than the revenue numbers suggest, and its lead investor argues the value was never in the legal data at all, but in the workflow scaffolding built on a firm's own documents. A fast follower can build that too.

And the founders' own answer to what the real moat is quietly gives the game away. Asked by EO what survives once the technology matures, Weinberg does not name a structure at all.

"If the models get really, really good, all traditional moats go away. And really, what matters the most is just... your team."Winston WeinbergCo-founder & CEO, Harvey

Team and execution are real things. But hiring is an operating skill anyone can copy, not a structure that defends you. If the honest answer to what the moat is is our people, then the structural moat is still hypothetical.

And then there was the market's reflex. One legal plugin from Anthropic was enough to knock legal tech stocks down hard. On the first try, investors priced this entire layer as something the labs could absorb.

None of this means Harvey loses. It means something narrower and more uncomfortable. Four years of fear bought time, position, brand, and speed, all of it real. They are also the very things that put Harvey in Gil's "just working" column, and Gil's own warning was that revenue cannot yet tell you which companies stay. Whether the fear bought a structure as well is the one thing none of the evidence shows yet.

Whichever case is right, it only settles whether the category survives. Whether Harvey is worth eleven billion dollars is a different question.

Ask Again in Two Years

The two cases above argue about whether the category survives. Even if it does, the price still has to be justified on its own.

Begin with the number, and with how soft it is. $11 billion against revenue puts the multiple somewhere between about 55 times, on an annualized 200 million, and 58 times, on the 190 million reported at the end of 2025. The 42 times you see quoted elsewhere was measured against the earlier 8 billion mark. The revenue figure itself slides between 190 million and significantly north of 200 million, depending on who is talking, so the multiple is a range, not a point.

A multiple like that says almost nothing about today's revenue. It is a bet on enormous future growth, and the fuel for that bet is the market's size. Harvey reaches single-digit percentages of ten million legal professionals, and the thirty billion dollars spent on legal technology is a sliver of a trillion-dollar industry.

But that logic cuts both ways, and it is Gabe Pereyra who hands you the knife. He told EO:

"If you look at most of these large industries, there's just room for everyone to be successful."Gabe PereyraCo-founder & President of Harvey

He means it as reassurance. He points to the database market. The big cloud providers all sell their own database infrastructure, and yet an independent company like MongoDB still grew into a large business because the market was large enough for a dominant incumbent and an independent player to thrive simultaneously.

But room for everyone is exactly the problem for a multiple of 55 times. A market big enough to guarantee Harvey a seat is big enough to seat the model providers next to it. The survival case and the market-size case both argue for the category. Neither one makes the argument for one company's valuation. That is the knot the number never unties.

So the honest place to end is here. Four years bought time and position. Whether that turns into a durable advantage comes down to one thing: whether the untrainable ground grows back faster than competitors and models can climb onto it.

And the whole argument has an expiry date. It holds right up until AI can fully replace human judgment. Past that point, the defense moves from the scarcity of judgment to sovereign, on-premise infrastructure, the banks and insurers that cannot touch cloud providers and will want the systems inside their own walls. The size of the market never guaranteed the moat would last. It only ever guaranteed the category would.

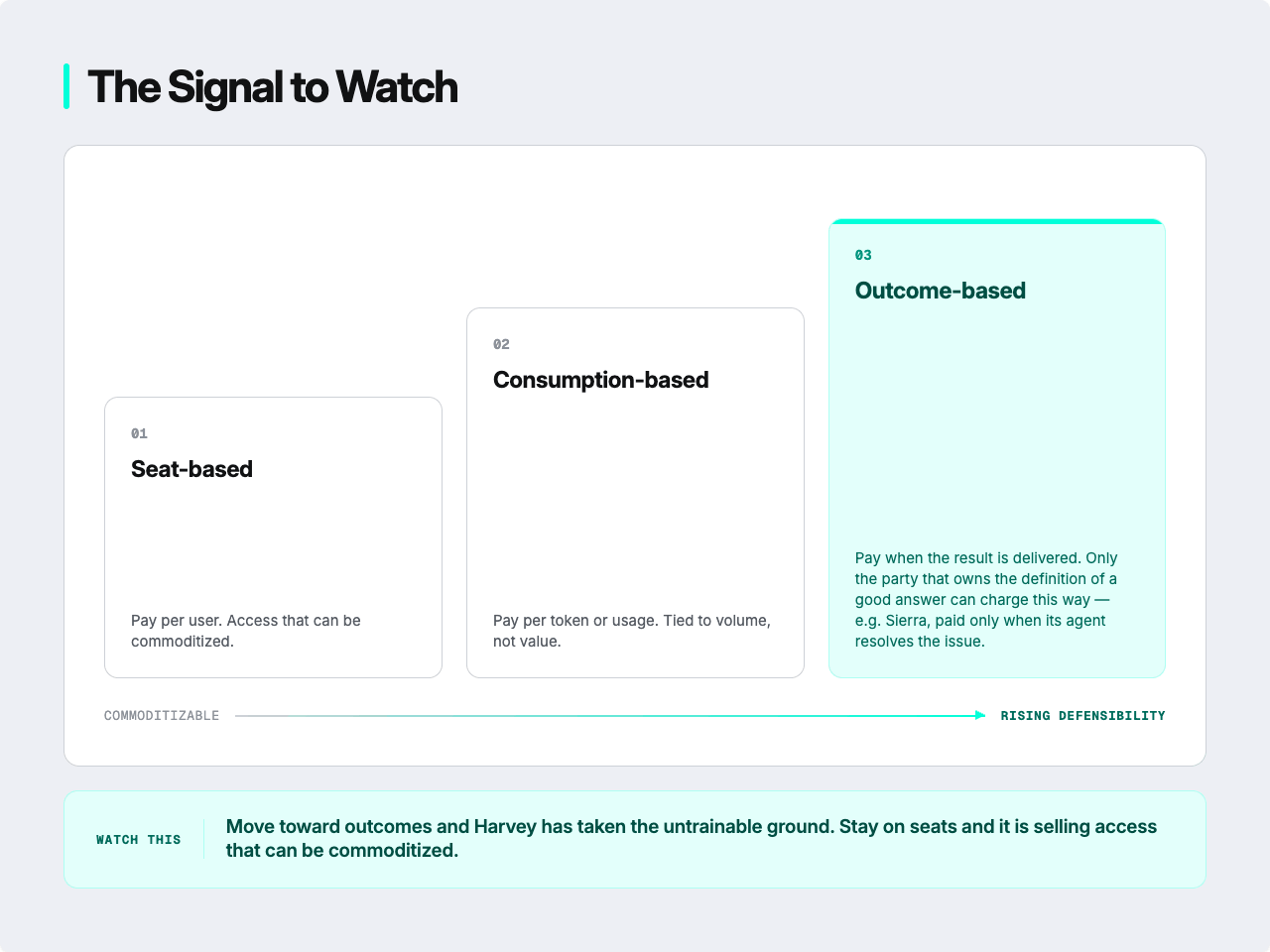

There is one signal worth watching, and it is concrete enough to be proven wrong. Watch whether Harvey's pricing moves from per-seat toward outcomes. Charging for outcomes is something only the party that owns the definition of a good answer can do. Sierra, the customer-support AI company, already works this way: it gets paid when its agent actually resolves a customer's issue and nothing when the problem goes to a human, which it can only do because it owns the definition of resolved.

The same logic can apply to legal tech, and Winston has already hinted at a move toward fixed fees and token-based pricing. If Harvey stays in seats, it is selling access that can be commoditized. If it moves to outcomes, it has actually taken the untrainable ground it talks about. Watch the multi-year expansion inside the Am Law 100, and watch the gap with Legora.

Four years early. Whether that was four years of advantage or four years of anxiety, the next two or three will tell. Guo calls the year's most-cited benchmark score a map of territory about to become worthless. An $11 billion valuation can age the same way.

💡

Further Reading

- $550 Million Says Legora Isn't Chasing Harvey. It's Betting on a Different Question., EO Magazine (March 2026)

- Harvey's Winston Weinberg: Why AI will force lawyers to change their fee structure, Financial Times (May 2026)

- Inside Harvey: How a first-year legal associate built one of Silicon Valley’s hottest startups, TechCrunch (November 2025)

- Harvey CEO Winston Weinberg Is Fixing Law’s ‘Broken Apprentice System’, Observer (September 2025)

- Harvey's founders say OpenAI is 'indirectly' its biggest competitor, Business Insider (October 2025)

Explore more