Mar 03, 2026

Early-Stage Investment Deals Will Rebound in 2026. Here Are 3 Reasons.

Three converging forces suggest the worst of the early-stage drought is over. The data makes the case.

Behind The Scenes

Is the Market Finally Recovering?

If you've been watching the venture market lately, you've probably gotten mixed signals. The downturn that started in 2022 never quite ended. And yet AI has injected a kind of historical excitement into the ecosystem that's hard to ignore. Mega-rounds are closing. Multistage firms are writing seed checks. IPOs are coming back.

So which is it: recovery, or noise?

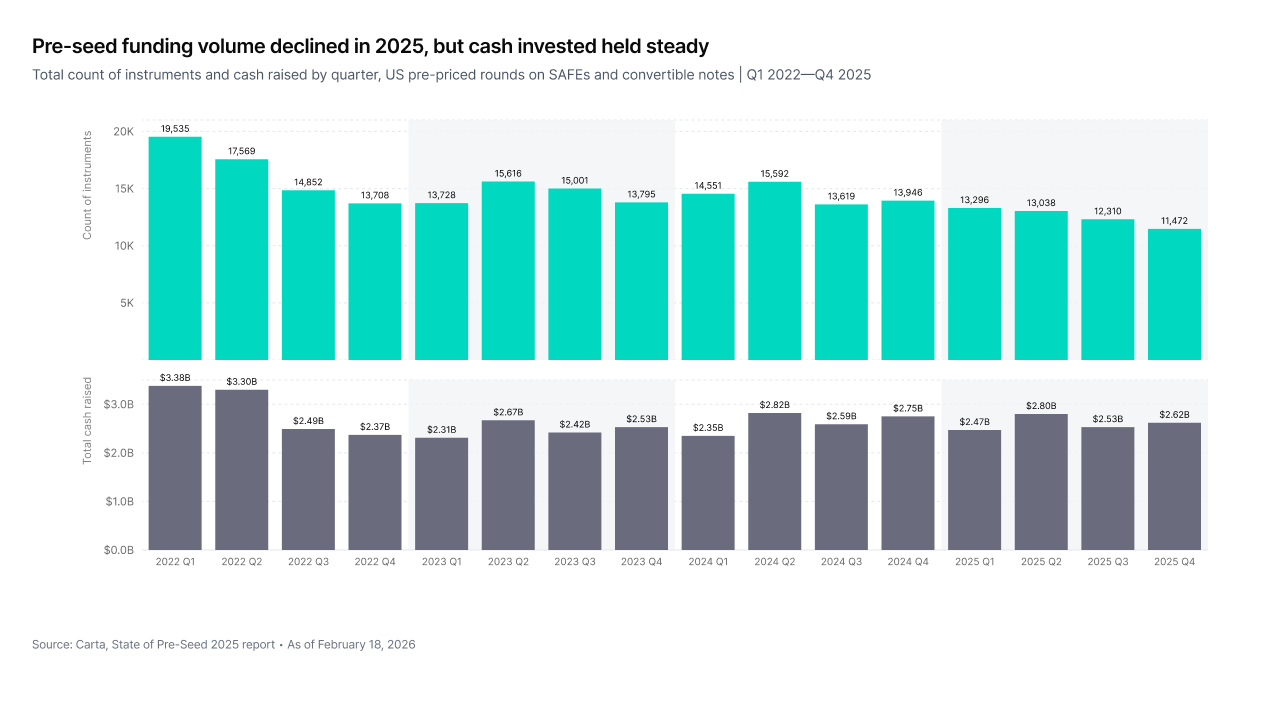

Even the data looks contradictory. According to Carta's State of Pre-Seed 2025 report, published in February 2026, the number of pre-seed instruments issued in Q4 2025 hit the lowest point in recent years. And yet the cash deployed that same quarter held steady at $2.62 billion, roughly in line with every quarter before it. Fewer deals, same capital. But both signals are real. This suggests increasing market concentration.

What's clearer now is where the momentum is actually building. The exit market began recovering in 2025, led by a resurgent IPO pipeline. That recovery is unlocking liquidity. And liquidity, historically, flows back into early-stage bets.

AI is accelerating that instinct, raising the perceived upside of getting into promising companies before they're priced accordingly. And the investors best positioned to act on all of this? Multistage firms, which can move capital from late-stage exits directly into seed and Series A deals without waiting for a new fund cycle.

Here are three reasons early-stage deal activity is set to rebound in 2026.

1. Total Liquidity Began to Recover

The venture capital ecosystem runs on a cycle: exits generate distributions to LPs, who then commit capital to new funds, which deploy into new deals. When that cycle stalls, as it did from 2022 to 2024, the entire market contracts. The good news is that in 2025, the cycle began to turn.

The IPO Market Builds Momentum

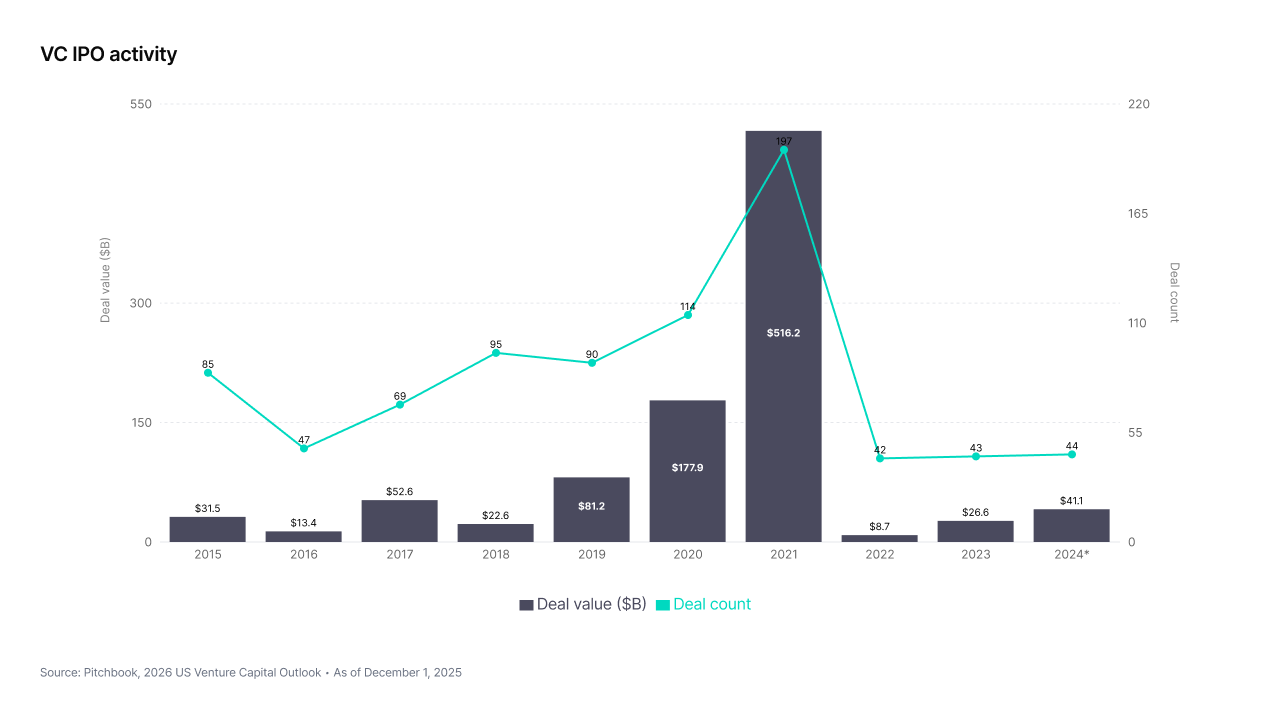

The most visible sign of recovery has been the reopening of the IPO window. After years of near-dormancy, IPO volumes and proceeds grew 20% and 84%, respectively, over the trailing 12 months through Q3 2025. The pipeline is finally moving.

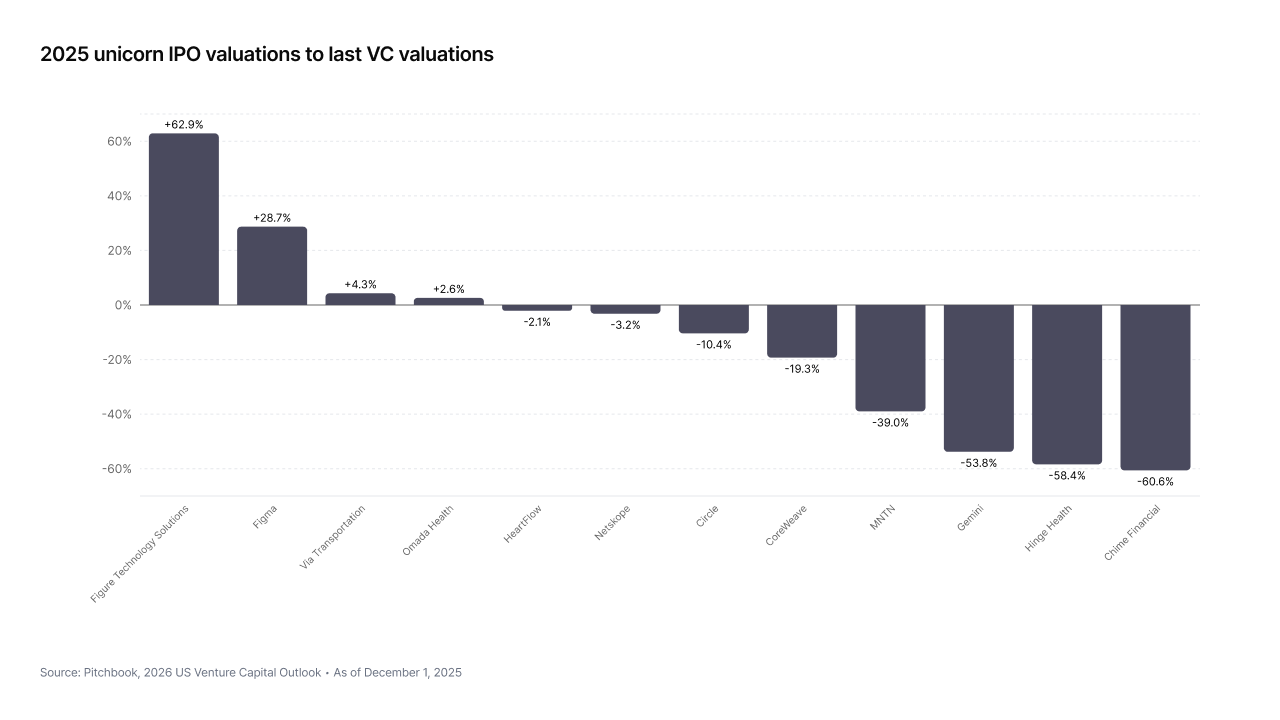

Critically, the playbook for going public has changed. Down-round IPOs, once considered taboo, became the norm in 2025. Two-thirds of unicorns that went public did so at valuations below their private market peak. The median U.S. IPO valuation for unicorns relative to their last VC valuation stood at just 0.9x year to date. But here is the counterintuitive part: many of these companies traded up substantially after listing, indicating strong public market appetite at realistic valuations.

Figma priced its shares at $33 on the NYSE in late July before more than tripling on its first day of trading, making it the largest tech IPO of the year. The Circle IPO followed, with the stablecoin issuer going public in conjunction with the passage of the GENIUS Act, a legislative tailwind that created a window of opportunity. In the defense and space sector, Voyager completed an oversubscribed IPO a month after the government increased investment in transformative space technology, followed by Firefly Aerospace two months later.

PitchBook's 2026 outlook projects 68 IPOs in its favorable scenario, a 44.7% increase from 2025's projected total, and 47 in its unfavorable scenario. Neither figure represents a breakout, but both signal a continuation of the recovery trajectory.

The most closely watched names on that list are OpenAI, Anthropic, and SpaceX. All three have signaled potential public listings in 2026, and all three are currently at the center of the biggest political flashpoint in tech: the U.S. military's adoption of AI. Whatever the outcome of those disputes, their IPO decisions will set the tone for the broader market.

OpenAI is currently the most likely to move first. On February 27, the company closed a $110 billion funding round backed by Amazon, Nvidia, and SoftBank at a pre-money valuation of $730 billion, the largest private financing in history. Hours later, it announced a Pentagon deal to deploy its models in classified networks, a move that signals its IPO runway is as clear as it has ever been.

The Secondary Market Surges

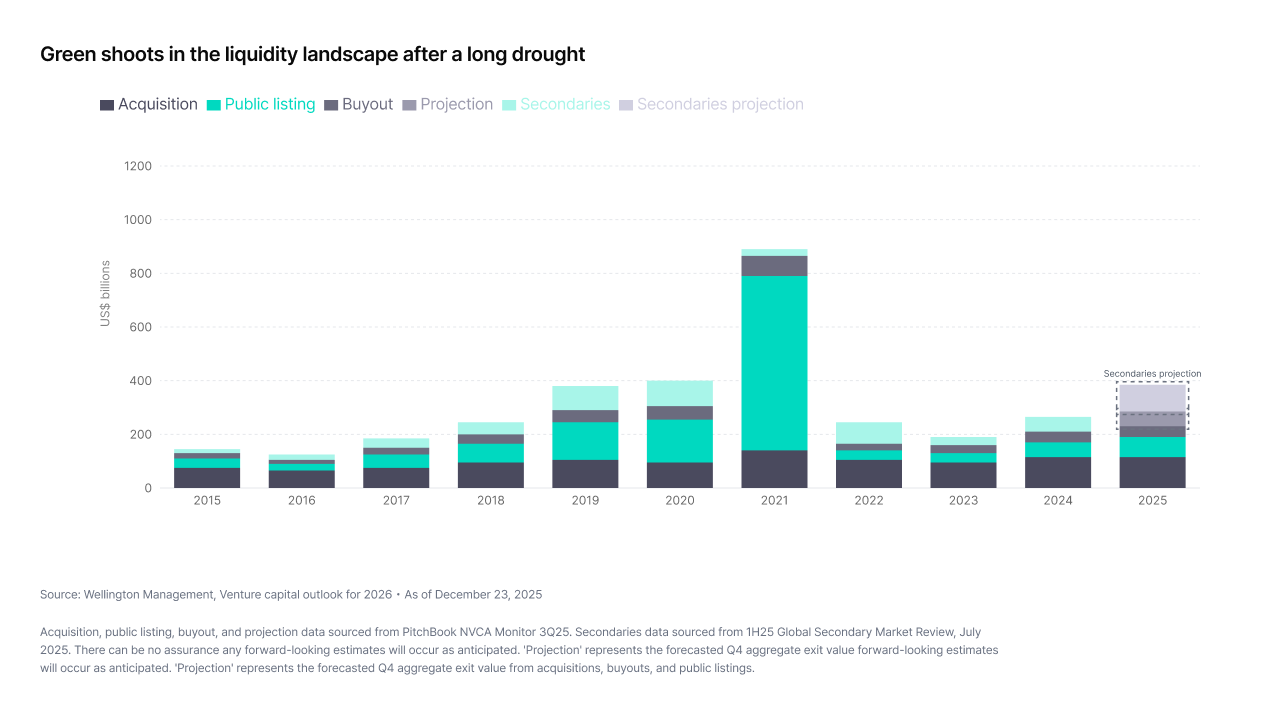

IPOs alone cannot solve the liquidity problem. With nearly half of unicorns being held for at least nine years, the venture market needs alternative exit pathways. That is exactly where secondaries have stepped in.

Secondary transactions ballooned to approximately $160 billion in 2024 and are projected to exceed $210 billion in 2025. The growth has been driven not only by volume but by a structural shift in how the market perceives secondaries. What was once a niche tool of last resort has become a core liquidity mechanism.

The clearest signal of this transformation came from Wall Street itself. In 2025, Goldman Sachs acquired Industry Ventures, Morgan Stanley purchased EquityZen, and Charles Schwab acquired Forge Global. These acquisitions signal that what was once a niche corner of alternative finance is becoming a mainstream liquidity mechanism.

Special purpose vehicles (SPVs) have become the fastest-growing access channel for retail engagement: compared with 2023 levels, the number of secondary SPVs is up 682%, and capital raised has surged 1,340%. This is not gradual growth; it is a structural shift in how private-market liquidity is created and distributed.

For the venture ecosystem, this matters because it means investors and founders no longer have to wait for an IPO or acquisition to achieve an exit. Liquidity can now be created at any stage, thereby reducing the friction associated with early-stage investing.

Why This Matters for Early-Stage Deals

The connection between exit market recovery and early-stage deal activity is direct and mechanical. When exits generate distributions, LPs redeploy a significant share of that returned capital into new funds. Historically, fundraising peaks and troughs have followed shifts in distribution yields by roughly one year. PitchBook's analysis shows that if 2025's exit momentum continues, fundraising could reach $100 billion to $130 billion in 2026.

But the more immediate effect is at the firm level. Multistage investors who realize gains from late-stage exits can immediately redeploy that capital into early-stage opportunities. This dynamic is explored further in Section 3.

2. AI Has Become a Defining Force in the Venture Market

AI is not just a hot investment theme. It is restructuring the venture capital market from the ground up, and its impact is most pronounced at the earliest stages of company formation.

The Scale of AI's Dominance

The scale of AI's takeover of venture capital is difficult to overstate. AI startups captured 65% of the total VC deal value in the U.S. through Q3 2025, up from 47.2% in 2024 and just 10% in 2015.

GAI companies raised $226 billion globally in 2025, accounting for 48% of total venture funding worldwide. The largest funding rounds of 2025 were, in fact, claimed entirely by AI companies: OpenAI ($41B), Anthropic ($32.5B), Scale ($14.8B), xAI ($12.8B), Databricks ($5B). These headline figures are skewed by the sheer size of late-stage AI rounds, but the dominance extends across all stages.

That trajectory matters as much as the absolute figure. Three years ago, AI was a significant but not dominant force in early-stage deal activity. Today, it is the defining one.

Where AI Is Reshaping Early-Stage Activity

The most compelling evidence of AI's impact on early-stage venture lies in three data points from PitchBook:

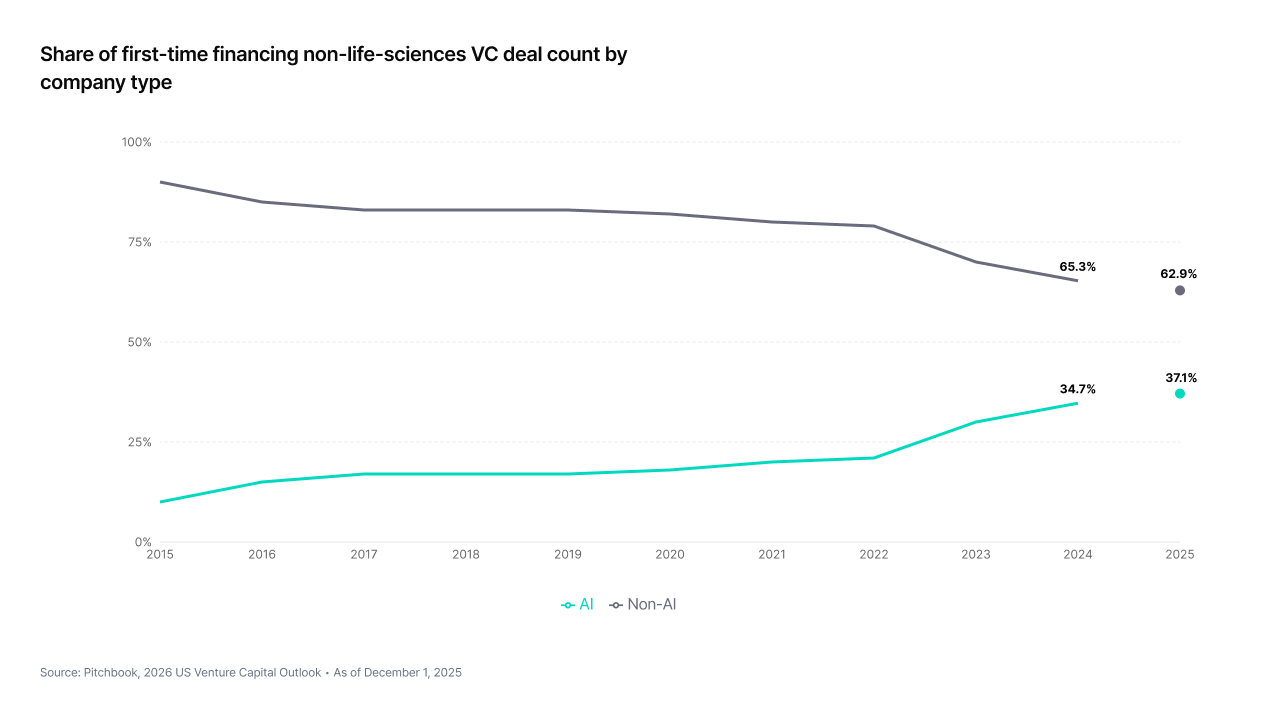

First, 37.1% of non-life-sciences first financings in 2025 were for AI companies, up from 21% in 2022. This is not a marginal shift; it represents a near-doubling in three years.

Second, the median age of AI startups receiving their first investment is 65% lower than that of non-AI startups. AI companies are getting funded faster because they can build and demonstrate value faster.

Third, the median time between rounds for AI companies is three months shorter than for non-AI companies, and the gap continues to widen. AI companies are not only starting faster but progressing through funding stages at an accelerated pace.

The result: AI is the primary engine behind first-time financing deal count approaching 2021's all-time high.

AI Lowers the Cost of Building a Company

Beyond attracting investor interest, AI is fundamentally reducing the cost and time required to build a startup. AI-powered tools for coding, design, customer support, and data analysis mean that founding teams can do more with fewer people and less capital. This has a direct effect on the early-stage market: lower startup costs mean more companies can reach the minimum viable product stage and attract seed funding.

PitchBook's analysis highlights this dynamic explicitly:

"AI has driven investor focus and shrunk the cost of building a company. This is not novel, as hype and costs are two directly relatable trends that can impact investment."Kyle StanfordDirector of Research, US Venture

The BVP Cloud 100 Benchmarks Report offers supporting evidence. AI companies now make up 42% of total Cloud 100 value, double the 21% share from just one year prior. More strikingly, AI companies reach the $100 million ARR milestone in an average of 5.7 years, compared to the overall Cloud 100 average of 7.5 years. Speed of value creation is compressing, and investors are responding.

Historical Context: AI's Unprecedented Share

No emerging technology has ever accounted for a larger share of total deal activity than AI does today. PitchBook draws a comparison to mobile, which made up about 20% of the deal count in early 2013, the previous high-water mark. AI currently stands at 35%, nearly double mobile's peak.

But the comparison understates AI's potential scope. Mobile was largely a platform shift within consumer technology. AI is increasingly an essential component across industries: biotech, enterprise productivity, climate tech, financial services, defense, and beyond. More than 40% of companies raising capital in 2025 were software companies, and AI will likely be adopted by a far wider range of companies. As AI continues to develop in functionality and accuracy, its use cases and venture capital share will only increase.

VCs interviewed by Crunchbase broadly expect total dollars deployed to increase by 10% to 25% in 2026 compared to 2025, with AI infrastructure, foundational models, and vertical AI applications gaining even more capital share. The flipside is that sectors without AI differentiation, including climate tech, crypto, and vertical SaaS, will face tighter purse strings.

3. Multistage Investors Are Increasingly Betting on the Earliest Deals

The third force driving the early-stage outlook is structural: the largest, best-capitalized venture firms are moving aggressively into seed and Series A rounds in ways they historically have not.

The Data Is Clear

Five of the 20 most active seed and early-stage investors in 2025 are multistage firms: Andreessen Horowitz(a16z), General Catalyst, Khosla Ventures, Sequoia Capital, and Lightspeed Venture Partners. Bessemer Venture Partners is not far behind. Together, these funds made over 400 seed and early-stage deals in 2025, their second-highest combined total ever, behind only 2021.

a16z alone invested in more than 300 seed and Series A deals since the beginning of 2024 as of November 2025. The firm's activity is emblematic of a broader strategic recalibration: multistage firms are no longer content to wait for later stage to enter a company. They want to be there from the beginning.

Why the Strategy Works

The conventional wisdom is that paying high valuations at the seed stage is risky. The data tells a different story. According to PitchBook, top-decile seed and Series A rounds by valuation exhibit higher annualized returns with lower loss rates than lower-valued rounds. Paying up early works, provided the investor has the capital to follow on.

And that is precisely the advantage multistage firms have. With fund sizes measured in the billions, they can deploy spray-and-pray tactics at the seed stage, but with less weight on the "pray" because of the sheer scale of their capital base. They can write checks into dozens or even hundreds of seed deals, knowing that the handful of winners will generate outsized returns, and they can guarantee their access to follow-on rounds.

This approach does two things simultaneously. It ensures the firm has a seat at the table for the best companies from day one. And it strengthens portfolio companies against competitors whose backers may not have as deep pockets.

The median seed deal size has nearly reached $4 million year to date, reflecting the inflation that multistage capital has brought to the earliest rounds. Fewer stakes are being acquired per deal, placing pressure on smaller managers to remain disciplined in pricing while competing against market giants.

a16z's $15 Billion Statement

Perhaps no single data point captures this trend better than Andreessen Horowitz's recent fundraise. The firm raised $15 billion in new funds, approximately 18% of all VC dollars raised in the U.S. in 2025. The allocation tells the story of where the firm sees opportunity:

The growth fund received approximately $6.75 billion for later-stage companies scaling rapidly. The American Dynamism fund took in about $1.176 billion for companies aligned with national strategic interests. The apps fund captured approximately $1.7 billion for consumer and enterprise startups, while the infrastructure fund received a similar amount for platform and foundational technology. The bio and health fund raised approximately $700 million, with the remaining $3 billion in flexible pools for opportunistic investments.

This is not just capital for deployment; it is a declaration of intent. a16z is building a capital structure designed to invest across the entire lifecycle of a company, from the first seed check to the pre-IPO growth round. And with the firm reportedly raising an additional $10 billion fund focused on AI and defense technology, the strategy is only accelerating.

What This Means for 2026

These three forces are not operating in isolation. They are reinforcing each other.

The exit market is returning capital to LPs and fund managers. That capital, combined with the gravitational pull of AI, is being redeployed at an accelerating pace. And the firms best positioned to deploy it quickly are the multistage investors who have built the infrastructure to invest at every stage, from the first seed check to the final pre-IPO round. Liquidity begets deployment, deployment fuels deal count, and AI provides the thesis that ties it all together.

A new pattern is emerging in Silicon Valley. As multistage firms push into the earliest stages, they are bringing more than capital. Fellowship programs, residencies, scout networks: infrastructure that was never available at the pre-seed level. Logos that once appeared on Series A term sheets are now showing up at demo days and pre-product conversations.

But for all these positive signals, the recovery is sharply uneven. As we noted in the introduction, venture dollars surged while deal count fell, a concentration dynamic that has only intensified. Startups outside the current wave, particularly those without an AI thesis, are unlikely to benefit. And the pressure extends beyond founders. Investors outside the largest multistage firms, especially smaller and emerging managers, face an equally difficult environment.

In other words, the recovery is selective. For founders who can position themselves within these currents, the on-ramp to venture capital is wider than it has been in three years. For those who cannot, the road ahead is harder than ever.

2026 is not a return to 2021. It is the year that defines the trajectory of the next decade of venture. The early-stage rebound is real. The question is who captures it.

Sources

- PitchBook, 2026 US Venture Capital Outlook, published December 1, 2025. Download

- Carmen, M., Craig, W., and Watson, M. (Wellington Management), "Venture Capital Outlook for 2026: 5 Key Trends," Harvard Law School Forum on Corporate Governance, December 23, 2025. Link

- CB Insights, State of Venture 2025 Report. Link

- Crunchbase, "VCs Expect More Funding, AI, IPO & M&A in 2026 Forecast." Link

- Bessemer Venture Partners, The Cloud 100 Benchmarks Report 2025. Link

- Crunchbase, "A16z Raises $15B In New Funds." Link

- Crunchbase, "Global Venture Funding In 2025 Surged As Startup Deals And Valuations Set All-Time Records." Link

- Carmen, M., Craig, W., and Watson, M. (Wellington Management), "Venture Capital Outlook for 2026: 5 Key Trends," Harvard Law School Forum on Corporate Governance, December 23, 2025. Link

- CB Insights, State of Venture 2025 Report. Link

- Crunchbase, "VCs Expect More Funding, AI, IPO & M&A in 2026 Forecast." Link

- Bessemer Venture Partners, The Cloud 100 Benchmarks Report 2025. Link

- Crunchbase, "A16z Raises $15B In New Funds." Link

- Crunchbase, "Global Venture Funding In 2025 Surged As Startup Deals And Valuations Set All-Time Records." Link

Explore more