May 27, 2026

Kalshi: What Investors Bet On Wasn't the Prediction Market

Inside Kalshi's $22B Series F

Raise Report

0:00 / 0:00

💡

At a Glance

- Company: Kalshi, the first regulated prediction market in the U.S.

- Co-founders: Tarek Mansour, Luana Lopes Lara

- Funding: $1B Series F at $22B valuation (May 2026, led by Coatue Management)

- Investors: Coatue, Sequoia Capital, Andreessen Horowitz, IVP, Paradigm, Morgan Stanley, ARK Invest, and others

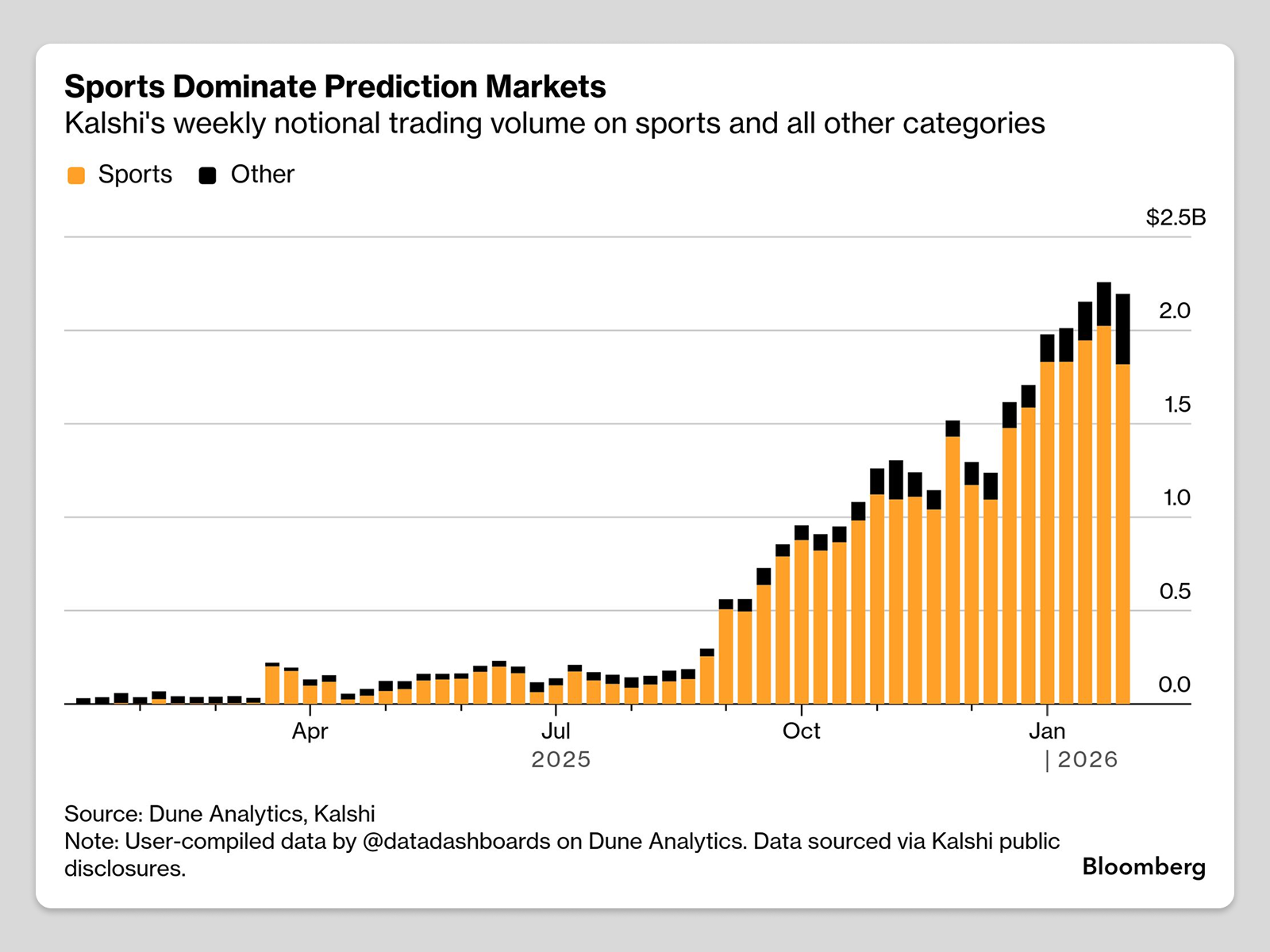

- Growth: $178B in annual trading volume (more than 3x in six months), over $1.5B in annual revenue, 2 million monthly active users

- Key Moment: The September 2024 victory in KalshiEx v. CFTC, which locked in a favorable precedent on the definition of "gaming." That precedent made the January 2025 sports market launch possible and led to the current structure, in which over 80% of trading happens in sports betting.

A Prediction Market on Paper, a Sportsbook in Practice

"Outside of AI, no company is growing like this."Lucas SwisherCoatue Management

In May 2026, Kalshi closed a $1B round led by Coatue Management at a $22B valuation. It was the company's fourth round in just one year. Annual revenue of $1.5 billion, two million monthly active users. Trading volume had more than tripled in six months to reach an annualized $178 billion.

But here is what Dan Schwarz, who designed Google's internal prediction market, said about the same company:

"It's really a sports gambling site with a thin layer of prediction market on top."Dan SchwarzCo-founder and CEO of FutureSearch

This comment reveals Kalshi's other face, the most contested startup of the moment.

More than 80 percent of Kalshi's trading volume comes from sports-event contracts. DraftKings and FanDuel now view Kalshi as a direct competitor and have launched prediction market products of their own.

A more cynical reading would be this: Kalshi makes its money not from the prediction-market vision but from sports betting dressed up as "event contracts." Investors weren't betting on a vision either; they were betting on a company that had found a workaround to operate a casino without paying taxes, and the $22B valuation is simply the price of that workaround.

But that reading alone can't account for the kind of persistence that made today's Kalshi possible. Trace the company's trajectory, and it becomes clear that Kalshi is a hybrid of two forces, a relentless vision and a clever regulatory strategy. Subtract either one, and the $22B valuation falls apart. What was once a small startup driven by a vision has become a large platform that now enjoys a privileged legal position.

For better or worse, this is a fight over whether Kalshi is remembered as the troublemaker the system absorbed or the definer of what came next. And investors, more coldly than anyone else, understand that these two faces can coexist, and that enormous value lives in that coexistence.

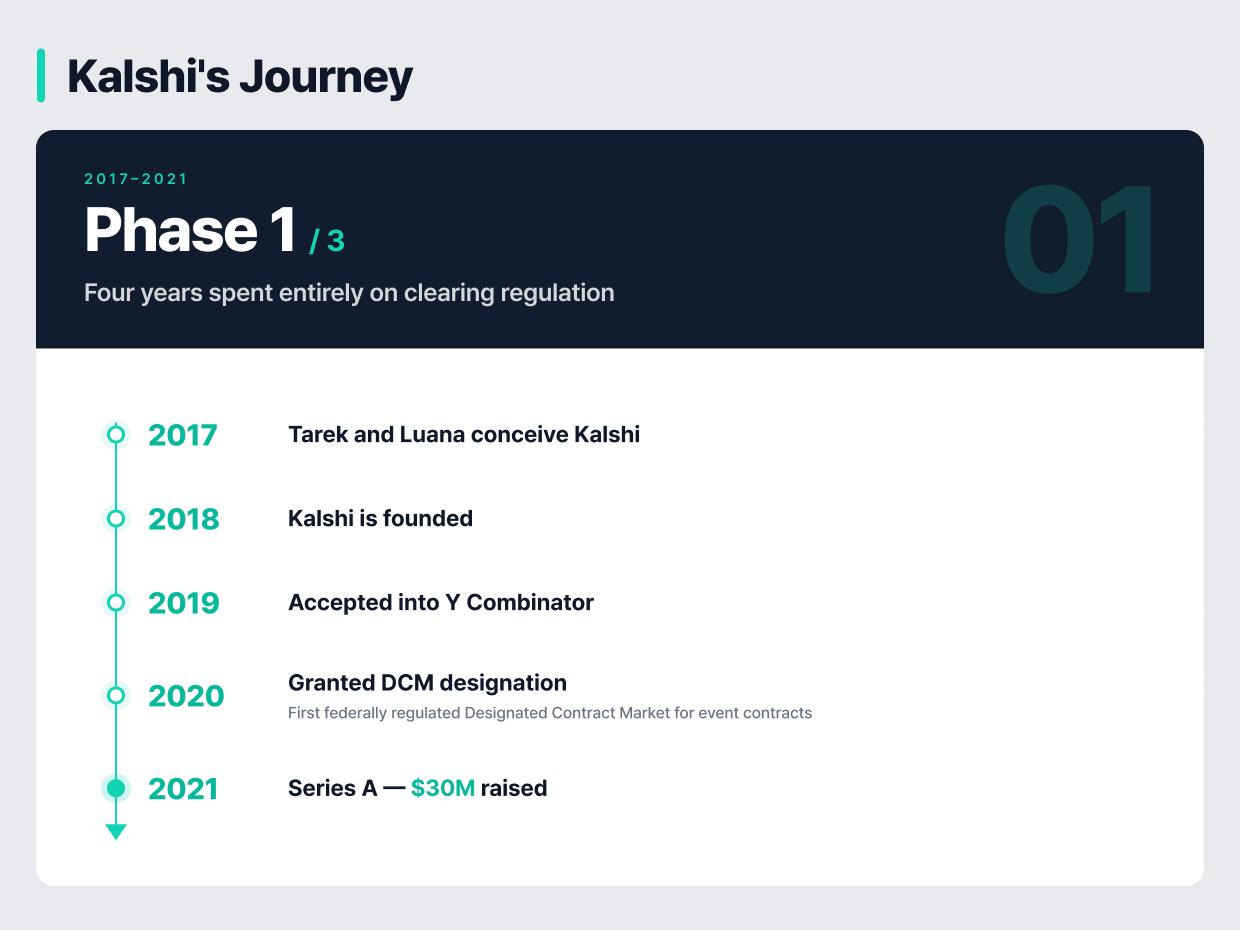

Phase 1 (2017–2021): The Moat Was Built in Filings, Not Code

The idea that 60 lawyers turned down

In the winter of 2017, when MIT seniors Tarek Mansour and Luana Lopes Lara first had the idea for Kalshi, they simply wanted to build a new kind of market. Tarek had observed something during his Goldman Sachs internship the previous summer: the trading desk wasn't focused on share prices. It was focused on events. Luana had seen the same thing at Bridgewater.

"I was an intern at Goldman Sachs in 2016. What surprised me was, investors really cared about was not what the price of a stock is. They really cared about whether Brexit was going to happen or not."Tarek MansourCo-founder and CEO of Kalshi

What the two of them quickly discovered was that no "market for events" had ever legally existed in the United States. Despite three decades of manifestos from academics, Ireland's Intrade had been blocked from U.S. access in 2013, and after that, the only legal option in the U.S. was PredictIt, a nonprofit academic market with an $850 betting cap.

The two of them contacted 60 lawyers to test the viability of the business. Not a single one told them, "This is possible."

"(At the YC hackathon) We presented, and we had a very janky demo; it was stablecoin-based at the time. And the first thing he said was, that's illegal."Luana Lopes LaraCo-founder of Kalshi

"I definitely remember that moment. This moment was foundational because it was when we decided to define one of the company's most important principles: we're going to do everything regulatory first." (Tarek)Tarek MansourCo-founder and CEO of Kalshi

The regulatory-first principle that Kalshi established during this period would become the decisive factor separating Kalshi's path from Polymarket's. Launch fast, outside of regulation. Or take the road no one had taken, build it legally, inside the United States. Of those two paths, Kalshi chose the latter.

YC, somewhat unexpectedly, took them in. Michael Seibel later described the decision this way.

"This sounds crazy, but these two MIT kids are really driven. Let's give them a shot."Michael SeibelPartner Emeritus at Y Combinator

Four Years of Filings, One License

The Kalshi that walked into its YC batch looked nothing like the other companies in the room. While other teams reported each week on 20% user growth and how much revenue they had pulled in, Kalshi reported on which lawyers they had met with and which documents they had filed.

"We'd talk to the government, and they'd send us a list of 20 concerns. We knew those concerns weren't justified, and we could prove it. So we'd do the data analysis, prove the legal theories, and send it back. Then they'd respond: 'We agree with your answers on one, two, and three. We have follow-up questions on four through twenty.' And we'd do it again."Luana Lopes LaraCo-founder of Kalshi

While the other companies in their batch were launching products and raising money, Kalshi was doing nothing but producing legal filings.

"The hard part about this regulatory first approach and being really committed to that regulatory first approach is you cannot show progress."

"It's kind of the unsexy parts of building a company. It was even more hard because some of our competitors launched and did it offshore without a license. I would say that was the hardest part of the path."Tarek MansourCo-founder and CEO of Kalshi

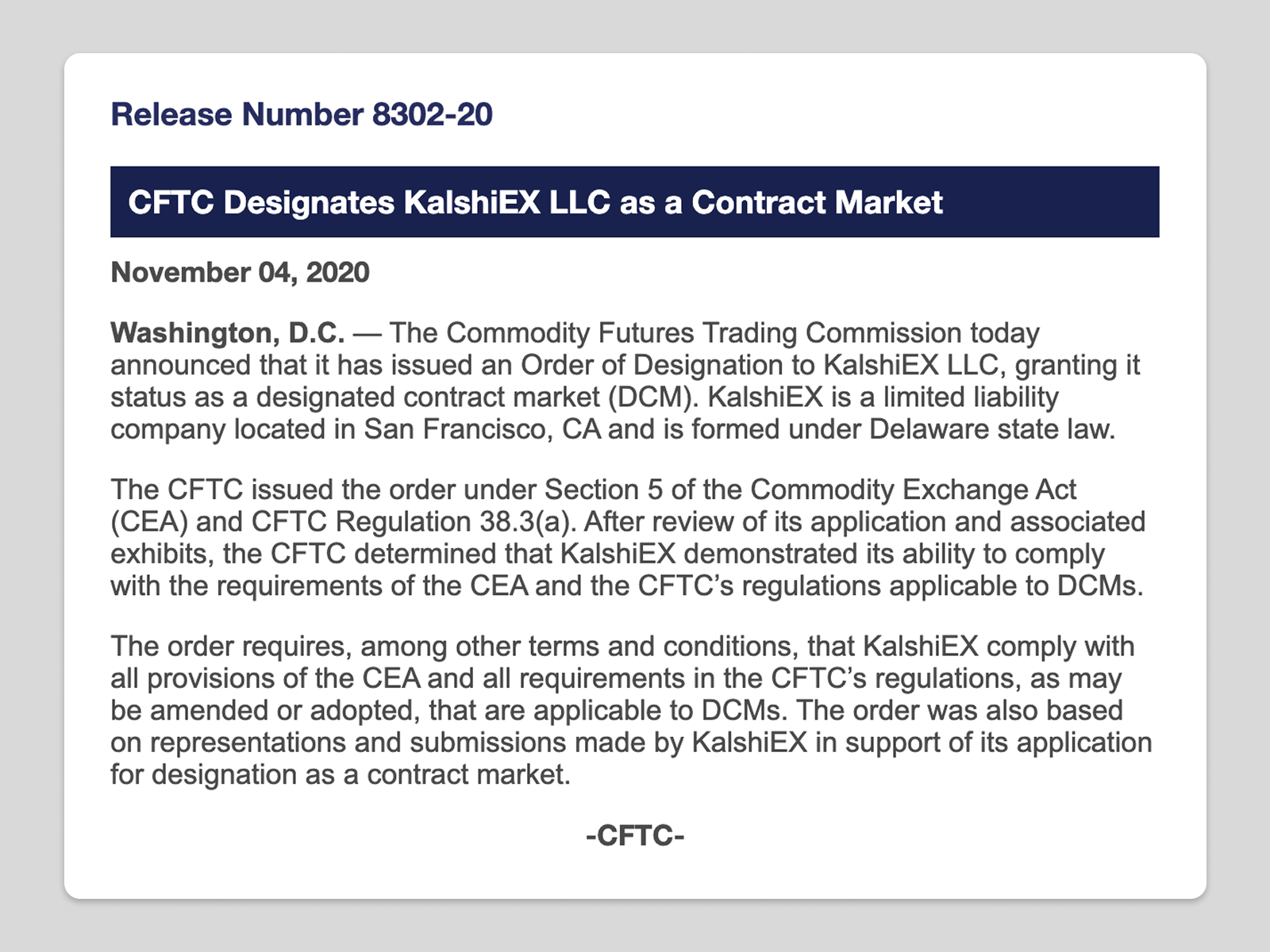

Their work finally paid off in late 2020, four years after the two of them first sketched the idea for Kalshi. On November 4, 2020, the CFTC announced it had granted Kalshi DCM (Designated Contract Market) status. In that moment, Kalshi became the first legally regulated U.S. exchange permitted to trade event contracts. They still had not launched a single product.

The Series A Bet: A License, Not a Product

The Series A, which came right after the DCM designation, drew Sequoia Capital and other early investors. Sequoia's Alfred Lin would go on to lead Kalshi through its Series D; during his PhD at Harvard, prediction markets were the subject of his research. Traditional finance figures like Charles Schwab and Henry Kravis also came in on this round.

By Tarek's recollection, there was almost nothing to show investors at that point. But the fact that the team had stayed locked on a single regulatory approval for four years and actually landed it became a very important proof of concept for Kalshi. Nothing demonstrates more clearly how mission-driven a team really is than that.

"One of the most fascinating parts of Tarek and Luana's journey is that if they weren't building Kalshi, they would probably be traders at Citadel. They wouldn't be entrepreneurs of another company."Alex ImmermanPartner of a16z

That alone made the bet worth it. Not the academic concept of "prediction markets" that scholars had championed for 30 years, but the legal category that first fit that concept into the U.S. legal system, more precisely, that first created the slot it could fit into.

Seen this way, Kalshi's real invention was not a product called "the prediction market." It was the legal construction itself: applying a DCM license to a new underlying called "events." And once that invention has been made, it doesn't have to be made again. This is why it took four years, and why it is a moat.

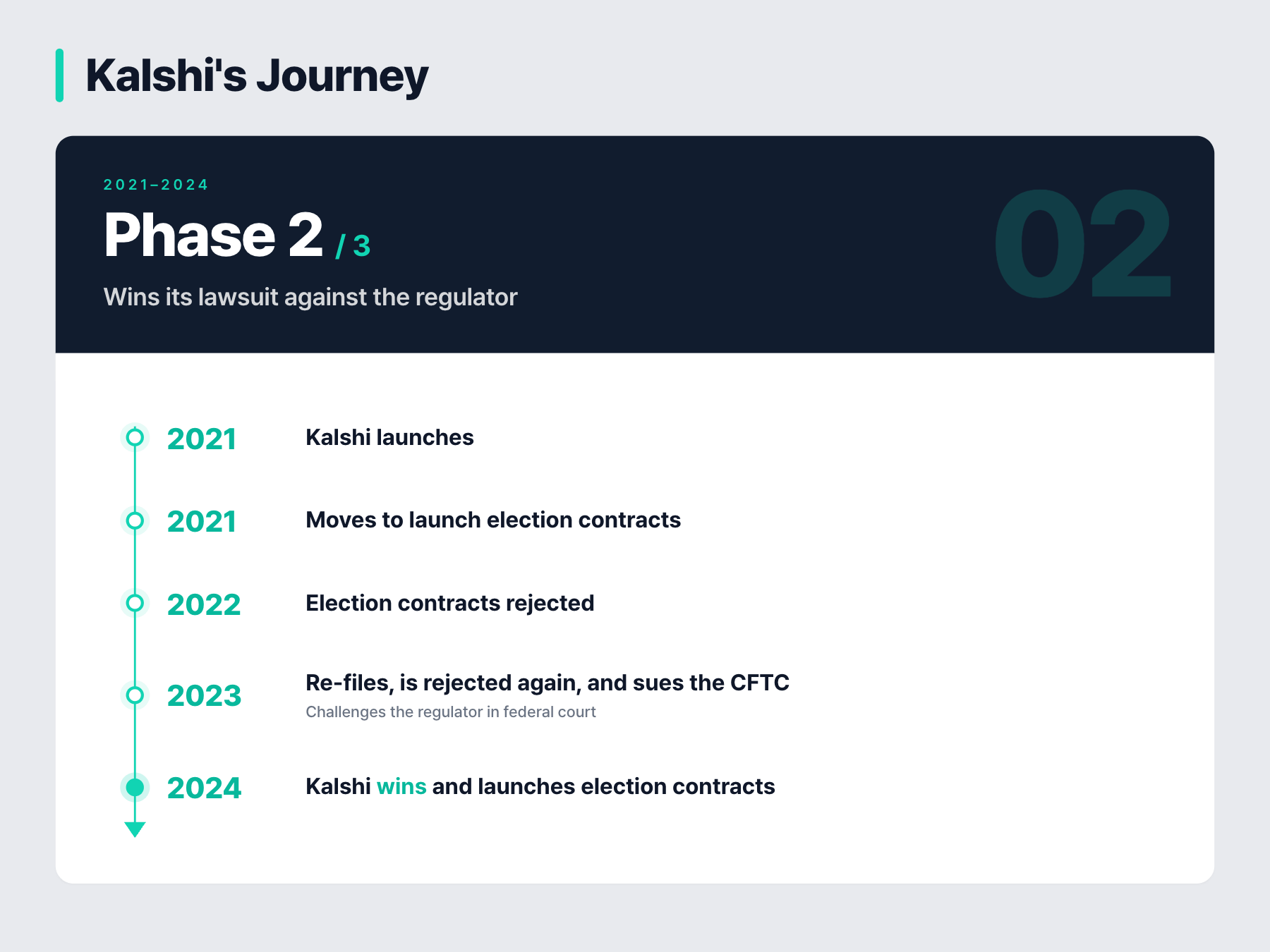

Phase 2 (2021–2024): Defining "Gaming" in Court

Election Markets: The Holy Grail

In 2021, Kalshi launched its platform and began operating an event-contract market. The number of hurricanes forming in the Atlantic, China's GDP growth rate, Oscar winners, and whether the federal government would shut down. Exactly the kind of market the 2008 academic manifesto had imagined.

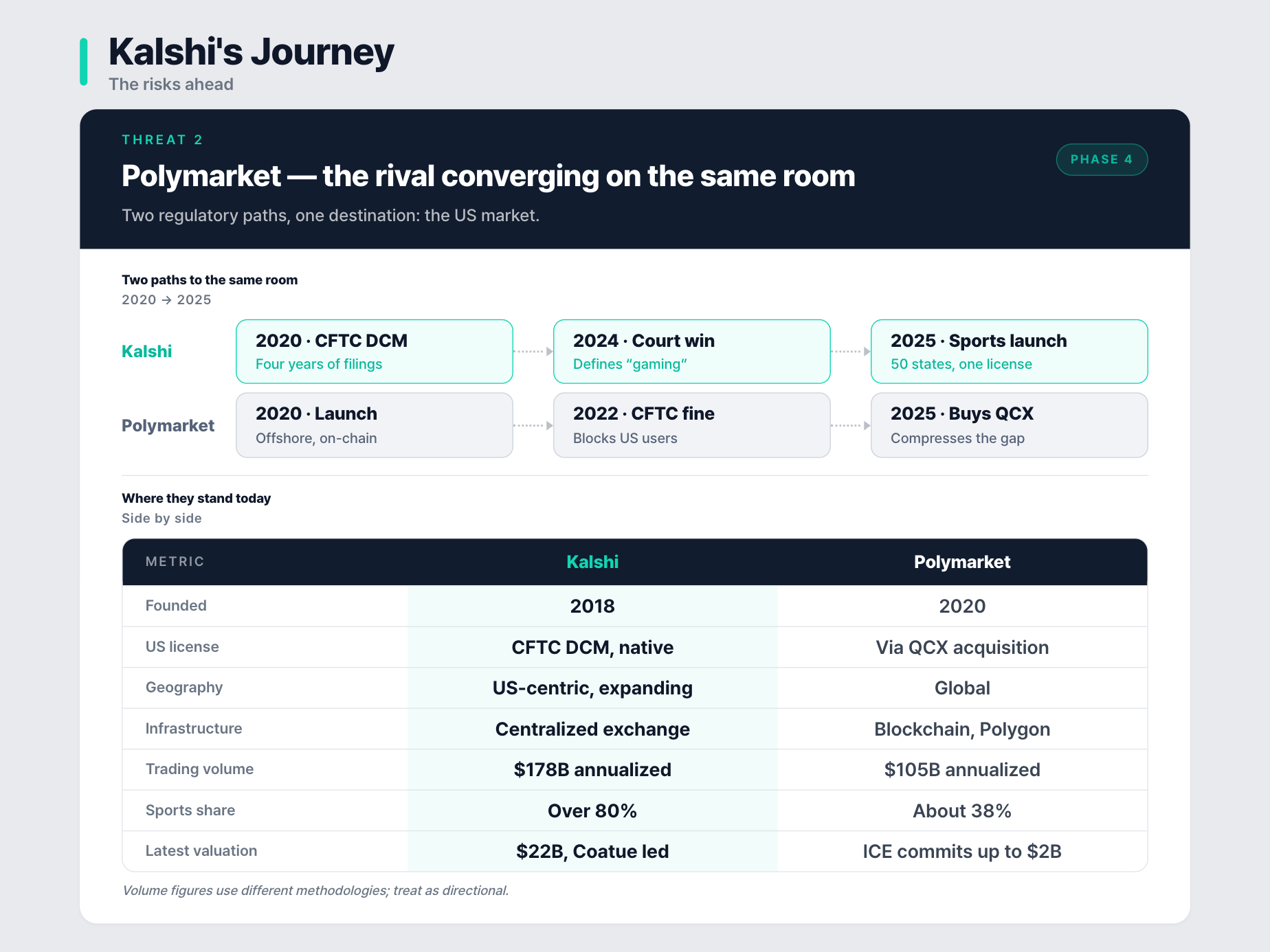

This was the period when Kalshi's and Polymarket's paths visibly split. Polymarket, founded by Shayne Coplan in 2020, started as a blockchain-based platform, but it operated without registering as a DCM and was hit with a $1.4 million fine and a cease-and-desist from the CFTC. After that, Polymarket chose to block U.S. IPs and headquarter itself in Panama. The "move fast outside of regulation" path.

Kalshi went in the exact opposite direction. It decided to take on the hardest category head-on, the very market that prediction-market scholars had spent 30 years championing above all others: election markets.

"We first tried to do elections at the end of 2021. It took a year, and they blocked it at the end of 2022. That was hard. A lot of the team left, investors stopped believing in it, and people were saying maybe we should pivot. But we tried again at the end of 2023, and the same thing happened. Blocked again."Tarek MansourCo-founder and CEO of Kalshi

Kalshi filed its first self-certification for an election market in 2022. The CFTC signaled opposition, and Kalshi withdrew it. Kalshi returned in June 2023 with Congressional Control Contracts, a yes/no event contract on which party would hold the majority in Congress.

The CFTC ruled the product fell under "unlawful activity" and "gaming" as defined in the CEA, and rejected it on a 3-1-1 vote in September 2023. Then-chair Rostin Behnam said the contract would "make the CFTC an election cop."

Kalshi then sued the CFTC. This was not a clean call for Kalshi either. The founders were in their mid-twenties, and Kalshi was still a small startup.

"We knew it would bring retaliation, death by a thousand paper cuts on every other project we had in the regulatory pipeline. But it was too important not to do it. There were two things that really mattered to us. One, these markets are the Holy Grail of prediction markets. They should be legal. And the other side is we knew we were right on the law."Luana Lopes LaraCo-founder of Kalshi

The Ruling That Changed Everything

Roughly a year later, on September 12, 2024, District Court Judge Jia M. Cobb issued her ruling in the case between the CFTC and Kalshi. The core finding was that elections cannot be treated as games, and that simply placing money on the outcome of an election does not constitute "involving" unlawful activity.

The CFTC had built its argument on the premise that "gaming" was equivalent to "gambling." The court read the two as meaningfully distinct and reasoned that when federal law uses the word "gaming," it refers to clear-cut game categories such as blackjack, roulette, and slot machines. The same meaning, the court held, had to apply here.

"For the foregoing reasons, the Court finds that Kalshi's congressional control contracts do not involve activity that is unlawful under any Federal or State law, nor do they involve gaming."Judge Jia M. CobbKalshiEx LLC v. CFTC, September 12, 2024

In October 2024, the Court of Appeals denied the CFTC's stay motion, and Kalshi immediately opened its election market.

With that, Kalshi defended the Holy Grail of prediction markets and won a favorable precedent on how "gaming" should be interpreted. The category Kalshi had built in Phase 1, "a federally licensed exchange for the events asset class," gained legal depth in Phase 2. And opening the election market carried a bigger impact than expected, because the moment Kalshi opened it, October 2024, was right before the U.S. presidential election.

Election Night Vindicates the Thesis

The 2024 election was a race between Donald Trump and Kamala Harris. In a tense political climate, traditional polls and mainstream outlets kept arriving at the same conclusion: "too close to call," "a dead heat." But prediction markets pointed to a Trump win earlier and with higher probability than the polls did.

On election night, before the major networks officially called the race, Kalshi's prices had already swung clearly toward Trump. The event gave Kalshi three things at once.

First, public proof that the data itself was useful, the moment a 30-year academic claim was validated on the biggest stage available. Second, a narrative for the incoming administration: "Prediction markets were the platform that told you first that you would win." Third, enormous traffic and a flood of new users.

"We got over 2 million customers in two weeks, I think. We did over 2 billion in volume. It was crazy. Everything engineering-wise was breaking. We've never gotten that many deposits like ever in the years of the company. But we were still a very small team. We were 20, 25 people."Luana Lopes LaraCo-founder of Kalshi

Tarek said they had to absorb a "100x" scale-up overnight. A team of barely 20 worked around the clock and rode out the painful growth. They added more than 2 million users in 2 weeks, and trading volume surpassed $2 billion. After eight years of work, Kalshi's curve had finally bent exponentially.

For context, Kalshi is believed to have raised a Series B during this Phase 2 stretch, though no official announcement was made. That detail itself is evidence that Kalshi was still operating closer to "survival mode" at this point.

Phase 3 (2025–2026): The Moat Becomes a Launchpad

One License, Fifty States, Zero Gaming Tax

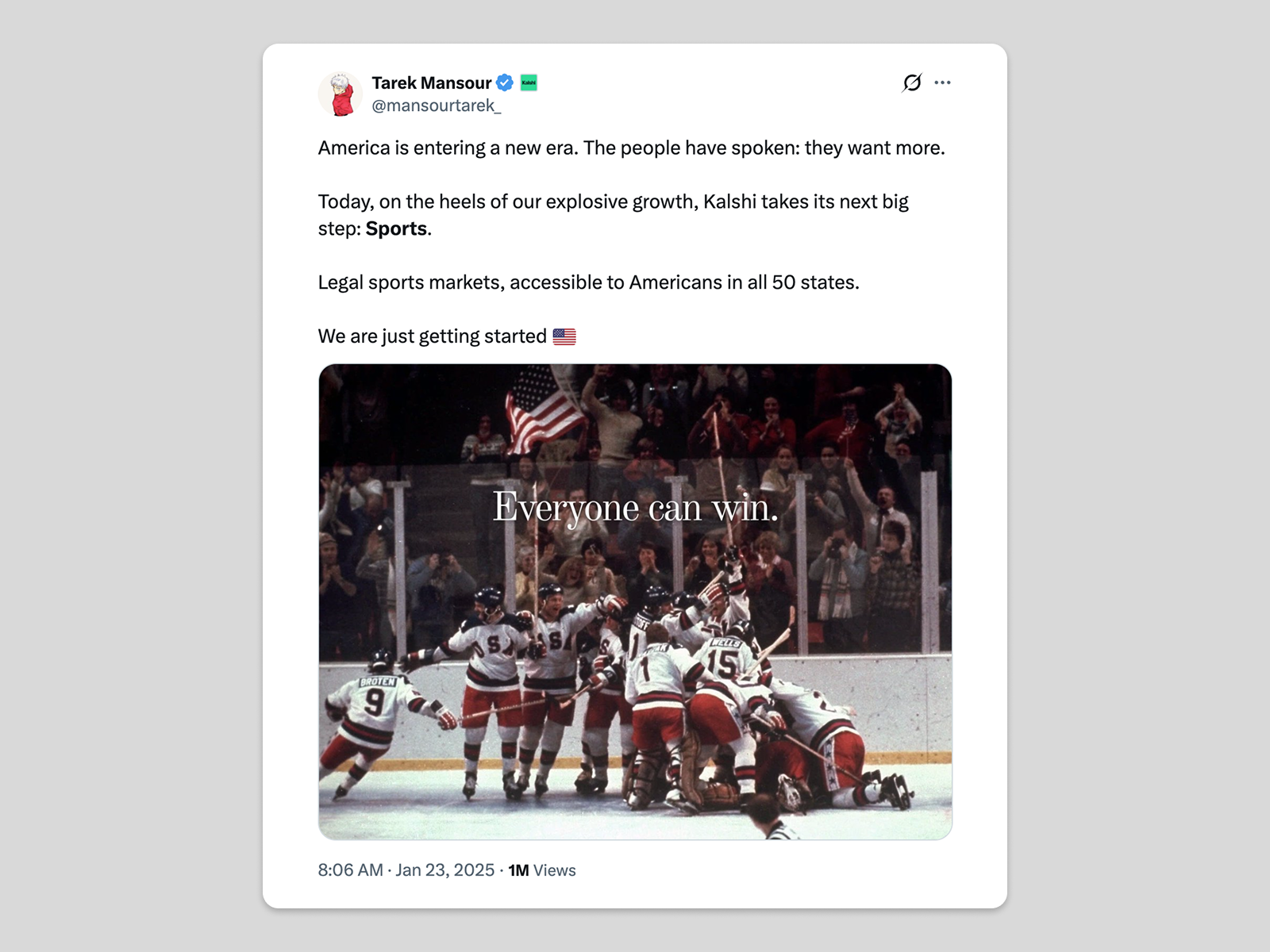

With the election market live, Kalshi turned to its next category: sports.

January 23, 2025. On this day, Kalshi launched sports event contracts across all 50 states, covering the Super Bowl, the AFC and NFC Championships, the NBA Finals, the Stanley Cup, and the NCAA men's basketball tournament. Kalshi had filed a self-certification for the sports event contracts, and the 90-day review window passed without incident.

It's hard to see the CFTC's clearance of Kalshi's most obviously "gambling-like" product as a coincidence. Three days before Kalshi filed its self-certification, on January 20, 2025, a new administration took office. On the same day, the CFTC's acting chair was replaced by Caroline Pham, who had abstained from the September 2023 vote rejecting the Congressional Control Contracts and was known to be favorable to prediction markets.

The press reported that Kalshi had built strong ties to the new administration. But the clearance was also the result of legal and political capital Kalshi had been accumulating for years. Since its founding, Kalshi has focused on a single thing: resolving its regulatory standing. In 2025 alone, it spent roughly $615K on federal lobbying. It also brought on Sara Slane, formerly of the AGA, Obama campaign manager Stephanie Cutter, and, after the election, Donald Trump Jr., building bridges to both parties at once. The board had included Brian Quintenz, a former CFTC commissioner, since 2021. The 2024 court win had added to Kalshi's stack of favorable precedent. None of this was the product of momentary luck.

So how did the sports event contracts perform?

The market was stunned. Sports betting had traditionally been classified as gambling, requiring state-by-state licensing, but Kalshi vaulted over that entire structure with a single CFTC license. The result was that Kalshi could skip the individual state licensing process altogether and even offer the product in states like California and Texas, where sports betting is illegal.

On top of that, Kalshi did not pay the gaming taxes that Bank of America estimates can run as high as 33%. Most states also cap sports betting at 21 and over, but because Kalshi was selling the product as an event contract, it was available to anyone 18 or older.

During Super Bowl week, Kalshi's new trader count surged 1,000 percent in seven days. Sports event contracts quickly grew to 80 percent of Kalshi's total trading volume, becoming the company's undisputed engine of growth. For Kalshi, regulation is no longer a wall to break through. It is a moat.

The Sports Wedge: Excuse or Strategy?

Is this the "prediction market" that academics championed for 30 years? Clearly not. But what's interesting is that even Justin Wolfers, the sharpest critic, concedes part of the logic.

"You need that honey to get the bees to come. Then the question is how much honey and how many bees do we really need?"Justin WolfersProfessor of Economics, University of Michigan

Alex Immerman of a16z, who led Kalshi's Series D, articulated the same logic in investor terms.

"Sports are a highly attractive customer acquisition wedge, and prediction markets provide a superior value proposition."

"Of course, we all want it to be more than sports. We think at end state, sports could be a meaningful portion of the business, 20-30% of volume, much less than it is today. But today, there's so much latent demand. Capturing the momentum from sports is so important. Capturing the momentum from sports allows you to convert users to other categories."Alex ImmermanPartner at a16z

Whether this is true or just an excuse will depend on what Kalshi builds next. Still, Kalshi's non-sports trading volume has reached an annualized $15–20 billion and has grown fivefold over the past year. In absolute terms, even setting sports aside, Kalshi is already a larger non-sports prediction market than Polymarket is.

In any case, Kalshi has entered a new phase, and its growth is staggering. That growth has translated directly into funding and valuation. In less than a year, the company has completed four funding rounds, with each round more than doubling the valuation of the one before. It is fair to say that today, outside of the leading group in AI, no company is growing faster.

What makes this more striking is that Kalshi appears to see all of this as a beginning, not an end. If sports is the "wedge" Alex describes, the exchange Kalshi is building is reaching for something much larger.

Phase 4: What the $22 Billion Is Really Pricing

Becoming the CME of a new asset class

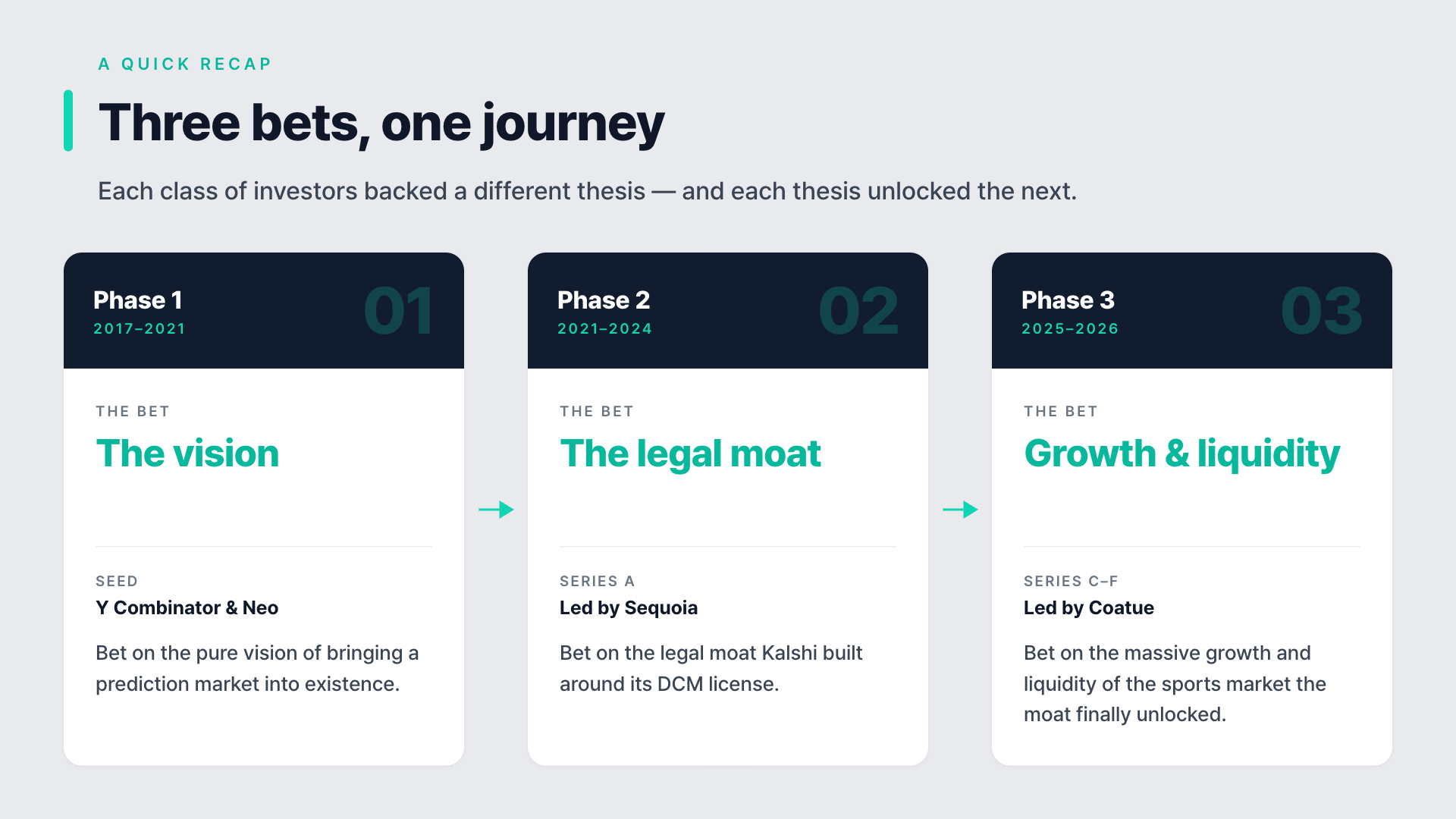

A quick recap.

In Phase 1, the seed investors, YC and Neo, bet on the pure "vision" of bringing a prediction market into existence. In Phase 2, the Series A investors led by Sequoia bet on the "legal moat" that Kalshi had built around its DCM license. In Phase 3, the large investors led by Coatue bet on the "massive growth and liquidity" of the sports market that the legal moat had finally made possible.

But judging by the profiles of the most recent round's investors and Kalshi's own moves, what they see in Kalshi's next chapter is clearly something larger.

"Kalshi plans to use the funds to further expand its services for corporate users, including more data integrations for trading firms and more block trading."The New York TimesMay 2026

"Institutional trading will be the overwhelming majority of our business within a few years."Tarek MansourCo-founder and CEO of Kalshi

In interviews, including one with EO, Kalshi has said the recently raised capital will be deployed to expand into the institutional market. Institutional trading volume has, in fact, risen 800 percent over the past six months. In May 2026, Kalshi executed its first custom block trade, beginning to handle negotiated transactions between institutions rather than retail flow. It has also signed a partnership with TradeWeb, a clearly institutional platform, unlike its previous retail partners Robinhood, Webull, and Coinbase.

This means Kalshi is trying to be more than just a platform for individual users. It is positioning itself as an "exchange", the venue through which other trading infrastructures access the event market.

If that is the case, the right comparable is not DraftKings (market cap roughly $16B). It is CME Group ($80B) and Intercontinental Exchange ($95B), the dominant U.S. exchanges for futures and equities, respectively. Each took decades to reach that position. If "events" is the next asset class to settle, and Kalshi becomes its CME, then $22 billion is the entry ticket, not the ceiling.

That Coatue led the round is itself a signal. Coatue began as a hedge fund and understands the exchange business. That Morgan Stanley and ARK joined is another piece. That ICE, the parent of the NYSE, committed up to $2B to Polymarket on the other side of the same trade is the loudest piece. None of these investors is paying for a betting board. They are pricing the on-ramp to an asset class.

Becoming the CME of a new asset class, or being the people who put the highest price tag on a sports betting site. That is what $22 billion is actually pricing.

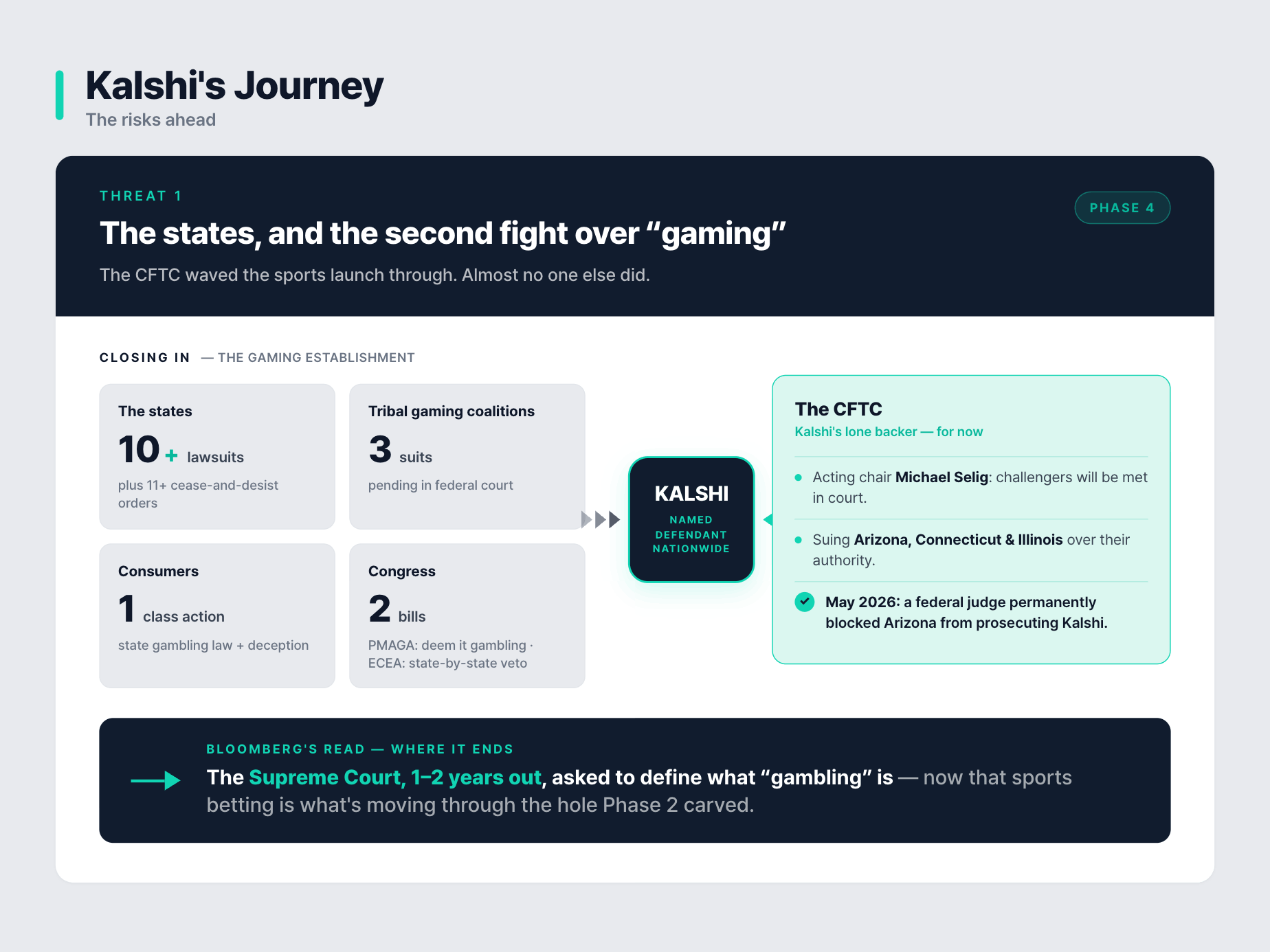

Threat 1: The States, and the Second Fight Over "Gaming"

Of course, the bigger the table, the bigger the risk, and the risks now facing Kalshi are on an entirely different scale than before. Two major threats are closing in. Each asks a different question about what Kalshi actually is.

The first is the backlash to the sports launch itself. The CFTC waved the product through; almost no one else did. The states losing gaming tax revenue and the licensed casinos losing market share have pushed back hardest, and Kalshi now finds itself the named defendant in legal fights spanning most of the country. It is Phase 2's courtroom war, scaled up.

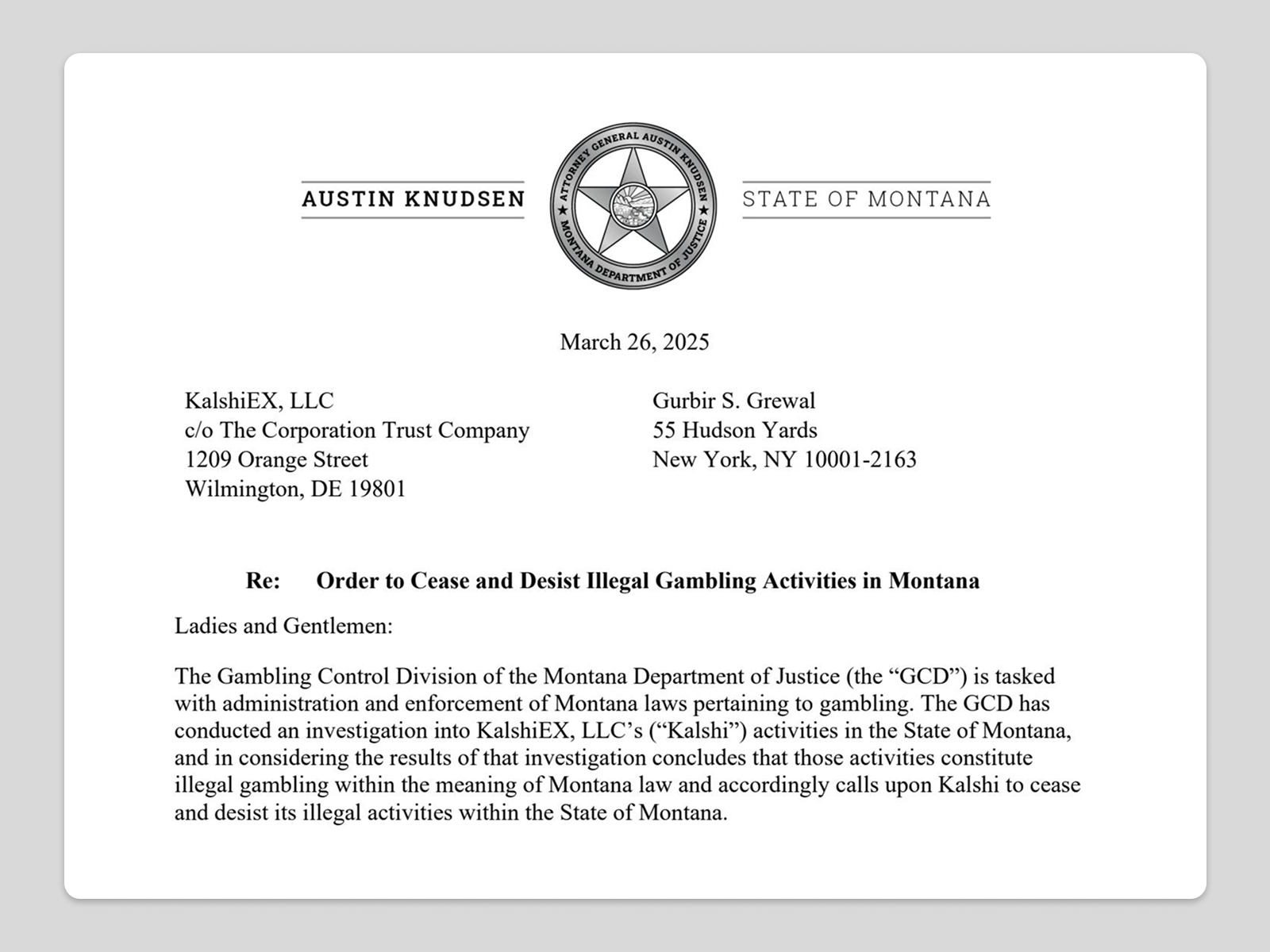

Kalshi is currently in litigation with more than ten states and has received cease-and-desist orders from at least eleven. Three suits brought by tribal gaming coalitions are pending. A consumer class action grounded in state gambling law and consumer deception is also live.

The legislative pressure mirrors the litigation. Two bills are before Congress. The Prediction Market Anti-Gambling Act (PMAGA) would classify prediction markets as gambling. The Event Contract Enforcement Act (ECEA) would give each state the authority to decide whether Kalshi can operate within its borders. Either, if passed, unwinds at least part of what Kalshi won in 2024.

The CFTC, for the moment, is on Kalshi's side. Acting chair Michael Selig has said publicly that those challenging the agency's authority will be met in court. The agency has filed its own suits against Arizona, Connecticut, and Illinois. And Kalshi is winning some of them. In May 2026, a federal judge permanently blocked Arizona from prosecuting the company under state gambling law.

Bloomberg's read is that this ends at the Supreme Court, one to two years out, with the Court being asked to define what gambling is. Phase 2's win defined "gaming" narrowly enough to fit a Kalshi-shaped hole. Phase 4 will decide whether that definition holds when sports betting, the single largest source of gaming tax revenue for U.S. states, is what is moving through the hole.

If it holds, Kalshi's regulatory moat in the U.S. becomes essentially permanent. If it doesn't, the structural advantage that made Phase 3 possible disappears, and Kalshi reverts to competing as one licensed operator among many.

Threat 2: Polymarket and the Bet ICE Already Made

If the states are asking whether Kalshi is gambling, Polymarket is asking whether Kalshi's moat actually matters.

What Phase 2 Kalshi won in court, Polymarket simply bought. Its 2025 acquisition of QCX, a CFTC-licensed entity, compressed four years of regulatory work into a single M&A transaction. The "Polymarket US" is now live.

What is more uncomfortable is that Polymarket is bringing two things into the U.S. that Kalshi does not have.

The first is the global brand. Through the 2024 U.S. election cycle, the graph that CNN, the BBC, the Financial Times, the Guardian, and Le Monde all cited was Polymarket's. The Dow Jones data partnership that lets the WSJ quote Polymarket probabilities in its own articles is, in practice, a formal stamp certifying "Polymarket equals trusted probability." Kalshi defended the holy grail in court. Polymarket became the number the world quotes.

The second is ICE. The New York Stock Exchange's parent company is committing up to $2B to Polymarket, which is not a normal venture investment. It is at the very top of the U.S. financial infrastructure stack, identifying which prediction market it wants to be the infrastructure for. The implication for Kalshi is hard to dismiss.

Widen the frame, and the gap shows up again. Kalshi's moat is calibrated for the U.S. system. None of those translates. To enter the UK, the EU, or Japan, Kalshi has to start from scratch in each jurisdiction. The work that took four years to do once in the U.S. would have to be repeated, in some form, dozens of times globally. Polymarket has spent those same four years building a global user base atop a blockchain that does not care about jurisdictions.

However, both threats were on the table when Coatue wrote the term sheet. The $22B is not the price of avoiding them. It is the price of betting that Kalshi is the company that ends up defining how they get resolved.

The Definer, or the Troublemaker

Disruption from startups always brings what no one quite expected.

Kalshi is no exception. What began in 2017 as two MIT seniors trying to build a market for events ended up as something larger and stranger: a company whose central act of creation was not a product but a legal category, and whose fight, from the first lawyer who said no to the appellate ruling that defined "gaming," was a fight with the regulatory architecture of American finance itself.

Carried to its end, that fight has put Kalshi in a position few startups ever reach. It is not iterating inside an existing system. It is breaking pieces of the system and rebuilding them.

The line between gambling and investing, blurred for two decades by options, meme stocks, and crypto, is now being drawn or erased in courtrooms where Kalshi is the named party. The category of "events" as a tradable asset class, something the U.S. financial system has not added in a hundred years, is being defined by whatever Kalshi's exchange ends up being.

If it wins, Kalshi enters history as the definer of those concepts. If it loses, it is remembered as a troublemaker that the system absorbed and moved past.

The critique may be aimed at the wrong target. The Kalshi that started in the language of prediction markets is now aimed at something adjacent to it: a category of its own, the U.S. exchange for an asset class called events. What Phase 4 will decide is whether that empty space becomes a real industry, and whether Kalshi sits at the top of it.

Either way, the more interesting thing to watch over the next two years is not Kalshi's valuation. It is which lines move, and where.

Watch the in-depth documentary about Kalshi on the EO YouTube channel!

💡

Further Reading

- KalshiEX LLC v. Commodity Futures Trading Commission, No. 1:23-cv-03257, D.D.C. (Cobb, J., September 12, 2024)

- CFTC Grants KalshiEX LLC Designated Contract Market Registration (CFTC, November 2020)

- The Promise of Prediction Markets (Arrow et al., Science, May 2008)

- There’s Still Time to Make Prediction Markets Useful (Bloomberg, May 2026)

- PREDICTION MARKETS (Wolfers)

- Tarek's AMA (Reddit, 2024)

Explore more